David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Franklin Electric Co., Inc. (NASDAQ:FELE) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Franklin Electric’s Debt?

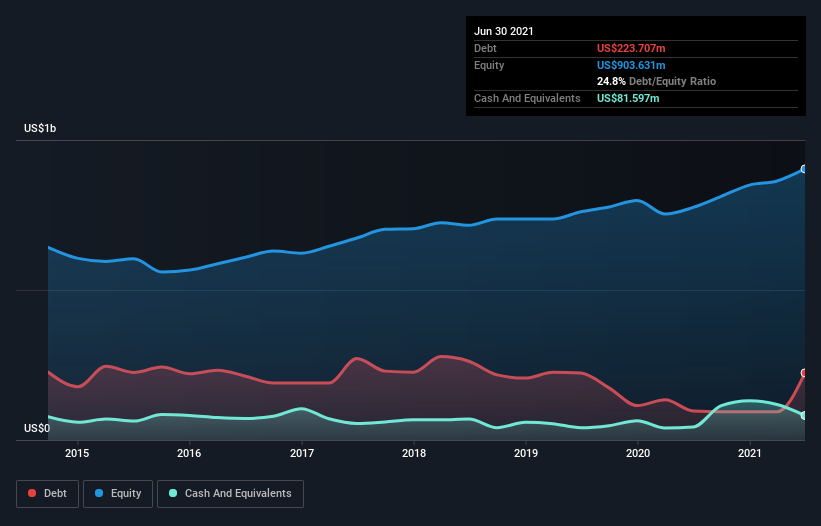

The image below, which you can click on for greater detail, shows that at June 2021 Franklin Electric had debt of US$223.7m, up from US$96.7m in one year. However, because it has a cash reserve of US$81.6m, its net debt is less, at about US$142.1m.

How Strong Is Franklin Electric’s Balance Sheet?

The latest balance sheet data shows that Franklin Electric had liabilities of US$387.0m due within a year, and liabilities of US$220.2m falling due after that. On the other hand, it had cash of US$81.6m and US$226.1m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$299.5m.

Of course, Franklin Electric has a market capitalization of US$3.96b, so these liabilities are probably manageable. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Franklin Electric has a low net debt to EBITDA ratio of only 0.71. And its EBIT easily covers its interest expense, being 34.3 times the size. So we’re pretty relaxed about its super-conservative use of debt. In addition to that, we’re happy to report that Franklin Electric has boosted its EBIT by 33%, thus reducing the spectre of future debt repayments. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Franklin Electric’s ability to maintain a healthy balance sheet going forward. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Happily for any shareholders, Franklin Electric actually produced more free cash flow than EBIT over the last three years. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Our View

Franklin Electric’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And that’s just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. It looks Franklin Electric has no trouble standing on its own two feet, and it has no reason to fear its lenders. For investing nerds like us its balance sheet is almost charming. The balance sheet is clearly the area to focus on when you are analysing debt.