Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Fortive Corporation (NYSE:FTV) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Fortive Carry?

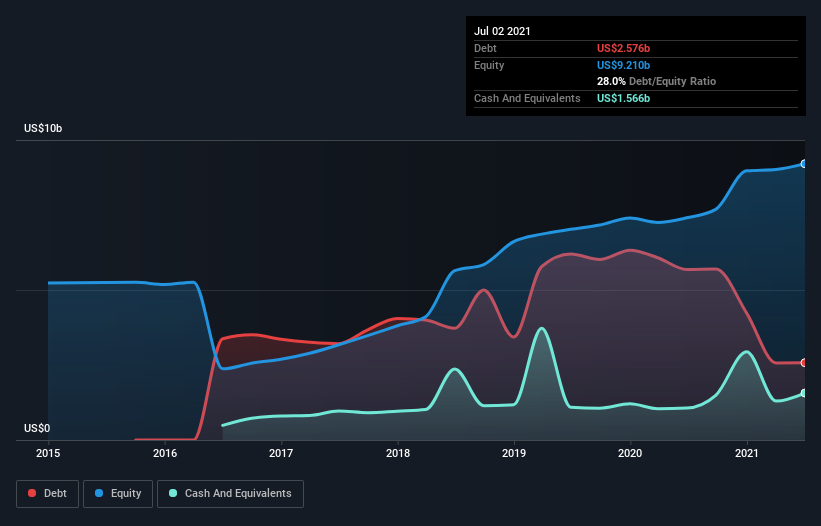

As you can see below, Fortive had US$2.58b of debt at July 2021, down from US$5.69b a year prior. However, because it has a cash reserve of US$1.57b, its net debt is less, at about US$1.01b.

A Look At Fortive’s Liabilities

We can see from the most recent balance sheet that Fortive had liabilities of US$2.57b falling due within a year, and liabilities of US$2.72b due beyond that. On the other hand, it had cash of US$1.57b and US$817.9m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$2.90b.

Since publicly traded Fortive shares are worth a very impressive total of US$26.3b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Looking at its net debt to EBITDA of 0.84 and interest cover of 6.5 times, it seems to us that Fortive is probably using debt in a pretty reasonable way. So we’d recommend keeping a close eye on the impact financing costs are having on the business. Better yet, Fortive grew its EBIT by 136% last year, which is an impressive improvement. That boost will make it even easier to pay down debt going forward. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Fortive can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Happily for any shareholders, Fortive actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Fortive’s conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And that’s just the beginning of the good news since its EBIT growth rate is also very heartening. Considering this range of factors, it seems to us that Fortive is quite prudent with its debt, and the risks seem well managed. So the balance sheet looks pretty healthy, to us. The balance sheet is clearly the area to focus on when you are analysing debt.