Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that First Solar, Inc. (NASDAQ:FSLR) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

What Is First Solar’s Debt?

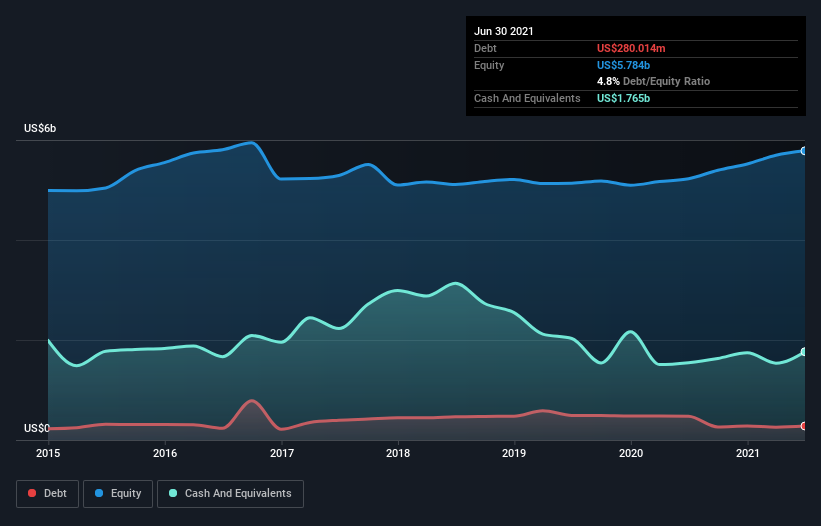

As you can see below, First Solar had US$280.0m of debt at June 2021, down from US$473.8m a year prior. But it also has US$1.77b in cash to offset that, meaning it has US$1.49b net cash.

How Strong Is First Solar’s Balance Sheet?

According to the last reported balance sheet, First Solar had liabilities of US$660.9m due within 12 months, and liabilities of US$803.9m due beyond 12 months. Offsetting this, it had US$1.77b in cash and US$597.6m in receivables that were due within 12 months. So it actually has US$898.2m more liquid assets than total liabilities.

This surplus suggests that First Solar has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that First Solar has more cash than debt is arguably a good indication that it can manage its debt safely.

In addition to that, we’re happy to report that First Solar has boosted its EBIT by 48%, thus reducing the spectre of future debt repayments. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if First Solar can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While First Solar has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last two years, First Solar saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that First Solar has net cash of US$1.49b, as well as more liquid assets than liabilities. And it impressed us with its EBIT growth of 48% over the last year. So we don’t have any problem with First Solar’s use of debt. The balance sheet is clearly the area to focus on when you are analysing debt.