Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Exelixis, Inc. (NASDAQ:EXEL) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Exelixis’s Debt?

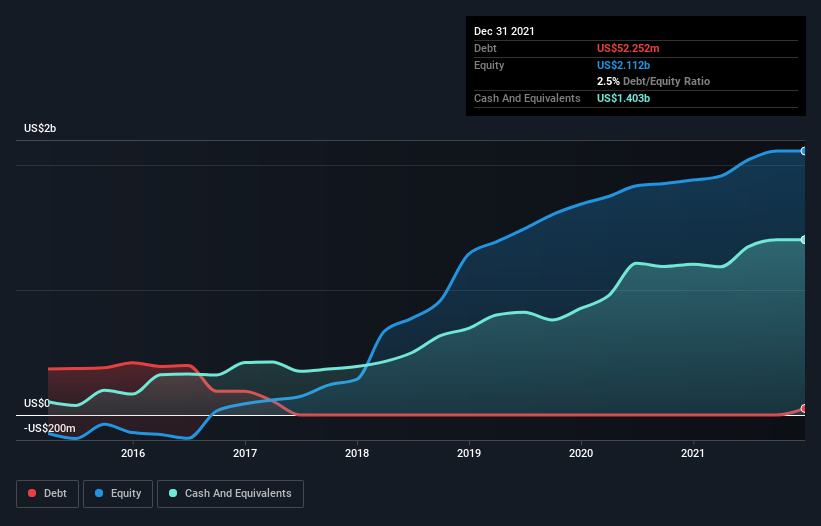

As you can see below, at the end of September 2021, Exelixis had US$52.3m of debt, up from none a year ago. Click the image for more detail. However, it does have US$1.40b in cash offsetting this, leading to net cash of US$1.35b.

A Look At Exelixis’ Liabilities

According to the last reported balance sheet, Exelixis had liabilities of US$269.5m due within 12 months, and liabilities of US$65.8m due beyond 12 months. Offsetting these obligations, it had cash of US$1.40b as well as receivables valued at US$182.1m due within 12 months. So it can boast US$1.25b more liquid assets than total liabilities.

It’s good to see that Exelixis has plenty of liquidity on its balance sheet, suggesting conservative management of liabilities. Given it has easily adequate short term liquidity, we don’t think it will have any issues with its lenders. Succinctly put, Exelixis boasts net cash, so it’s fair to say it does not have a heavy debt load!

Better yet, Exelixis grew its EBIT by 154% last year, which is an impressive improvement. That boost will make it even easier to pay down debt going forward. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Exelixis can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Exelixis has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Exelixis actually produced more free cash flow than EBIT over the last three years. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Summing up

While it is always sensible to investigate a company’s debt, in this case Exelixis has US$1.35b in net cash and a decent-looking balance sheet. And it impressed us with free cash flow of US$275m, being 126% of its EBIT. The bottom line is that we do not find Exelixis’s debt levels at all concerning. When analysing debt levels, the balance sheet is the obvious place to start.