Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Eagle Materials Inc. (NYSE:EXP) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Eagle Materials’s Net Debt?

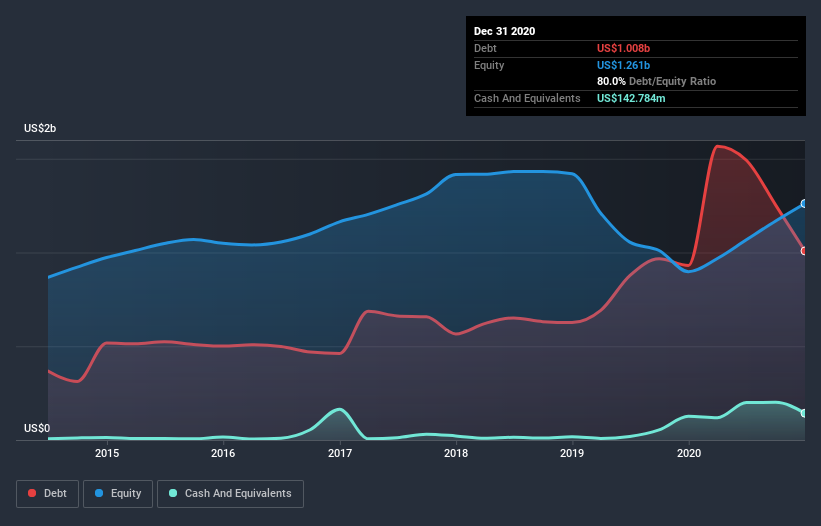

As you can see below, at the end of December 2020, Eagle Materials had US$1.01b of debt, up from US$930.6m a year ago. Click the image for more detail. However, it also had US$142.8m in cash, and so its net debt is US$865.6m.

How Strong Is Eagle Materials’ Balance Sheet?

We can see from the most recent balance sheet that Eagle Materials had liabilities of US$163.1m falling due within a year, and liabilities of US$1.30b due beyond that. Offsetting these obligations, it had cash of US$142.8m as well as receivables valued at US$144.4m due within 12 months. So its liabilities total US$1.18b more than the combination of its cash and short-term receivables.

Given Eagle Materials has a humongous market capitalization of US$11.5b, it’s hard to believe these liabilities pose much threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Eagle Materials’s net debt of 1.8 times EBITDA suggests graceful use of debt. And the alluring interest cover (EBIT of 8.4 times interest expense) certainly does not do anything to dispel this impression. We note that Eagle Materials grew its EBIT by 29% in the last year, and that should make it easier to pay down debt, going forward. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Eagle Materials can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Happily for any shareholders, Eagle Materials actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Eagle Materials’s conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And the good news does not stop there, as its EBIT growth rate also supports that impression! Looking at the bigger picture, we think Eagle Materials’s use of debt seems quite reasonable and we’re not concerned about it. After all, sensible leverage can boost returns on equity. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. We’ve identified 4 warning signs with Eagle Materials , and understanding them should be part of your investment process.

If you’re interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.