Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Dycom Industries, Inc. (NYSE:DY) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Dycom Industries’s Net Debt?

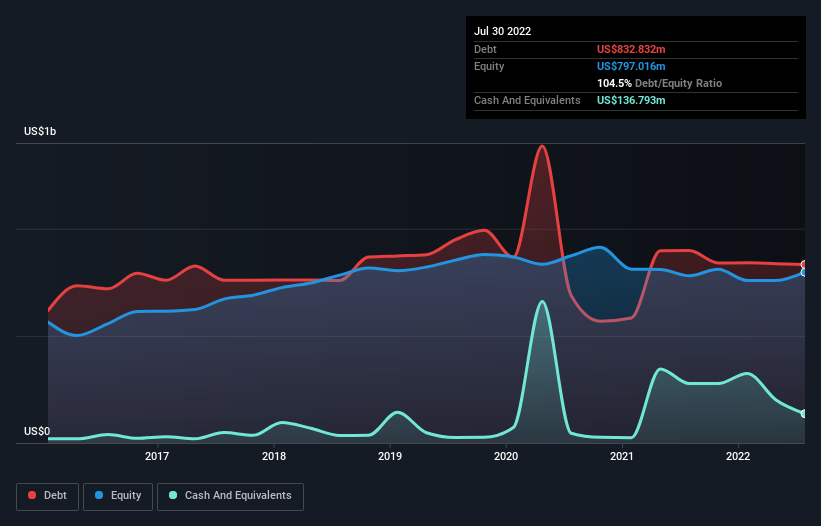

The image below, which you can click on for greater detail, shows that Dycom Industries had debt of US$832.8m at the end of July 2022, a reduction from US$897.8m over a year. However, it does have US$136.8m in cash offsetting this, leading to net debt of about US$696.0m.

A Look At Dycom Industries’ Liabilities

We can see from the most recent balance sheet that Dycom Industries had liabilities of US$432.1m falling due within a year, and liabilities of US$977.2m due beyond that. Offsetting this, it had US$136.8m in cash and US$1.17b in receivables that were due within 12 months. So it has liabilities totalling US$101.8m more than its cash and near-term receivables, combined.

Given Dycom Industries has a market capitalization of US$3.21b, it’s hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Dycom Industries’s net debt is sitting at a very reasonable 2.4 times its EBITDA, while its EBIT covered its interest expense just 3.8 times last year. In large part that’s due to the company’s significant depreciation and amortisation charges, which arguably mean its EBITDA is a very generous measure of earnings, and its debt may be more of a burden than it first appears. Importantly, Dycom Industries grew its EBIT by 73% over the last twelve months, and that growth will make it easier to handle its debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Dycom Industries can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Happily for any shareholders, Dycom Industries actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Dycom Industries’s conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. But, on a more sombre note, we are a little concerned by its interest cover. Looking at the bigger picture, we think Dycom Industries’s use of debt seems quite reasonable and we’re not concerned about it.