Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Dow Inc. (NYSE:DOW) makes use of debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Dow’s Debt?

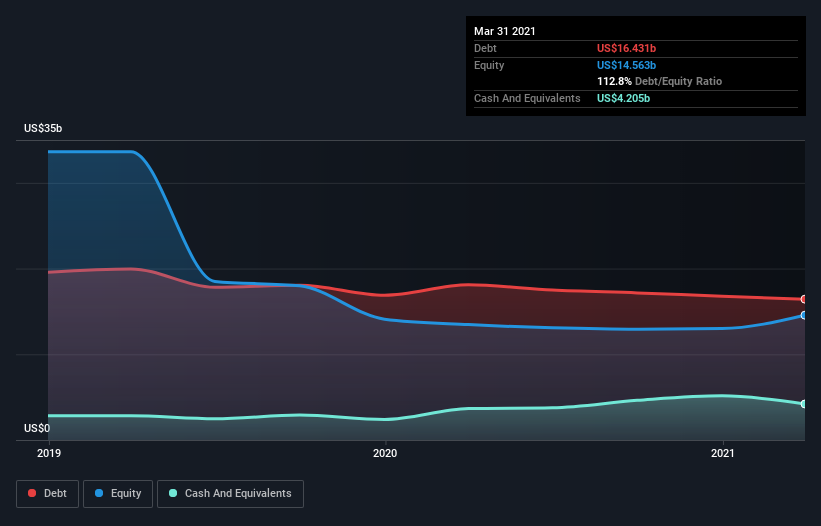

As you can see below, Dow had US$16.4b of debt at March 2021, down from US$18.1b a year prior. On the flip side, it has US$4.21b in cash leading to net debt of about US$12.2b.

A Look At Dow’s Liabilities

We can see from the most recent balance sheet that Dow had liabilities of US$11.4b falling due within a year, and liabilities of US$34.5b due beyond that. Offsetting these obligations, it had cash of US$4.21b as well as receivables valued at US$8.35b due within 12 months. So it has liabilities totalling US$33.3b more than its cash and near-term receivables, combined.

This is a mountain of leverage even relative to its gargantuan market capitalization of US$47.4b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Dow has net debt worth 2.1 times EBITDA, which isn’t too much, but its interest cover looks a bit on the low side, with EBIT at only 3.8 times the interest expense. While that doesn’t worry us too much, it does suggest the interest payments are somewhat of a burden. The bad news is that Dow saw its EBIT decline by 20% over the last year. If earnings continue to decline at that rate then handling the debt will be more difficult than taking three children under 5 to a fancy pants restaurant. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Dow can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Dow generated free cash flow amounting to a very robust 82% of its EBIT, more than we’d expect. That positions it well to pay down debt if desirable to do so.

Our View

Neither Dow’s ability to grow its EBIT nor its interest cover gave us confidence in its ability to take on more debt. But the good news is it seems to be able to convert EBIT to free cash flow with ease. Taking the abovementioned factors together we do think Dow’s debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn’t really want to see it increase from here. When analysing debt levels, the balance sheet is the obvious place to start.