Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Despegar.com, Corp. (NYSE:DESP) does carry debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

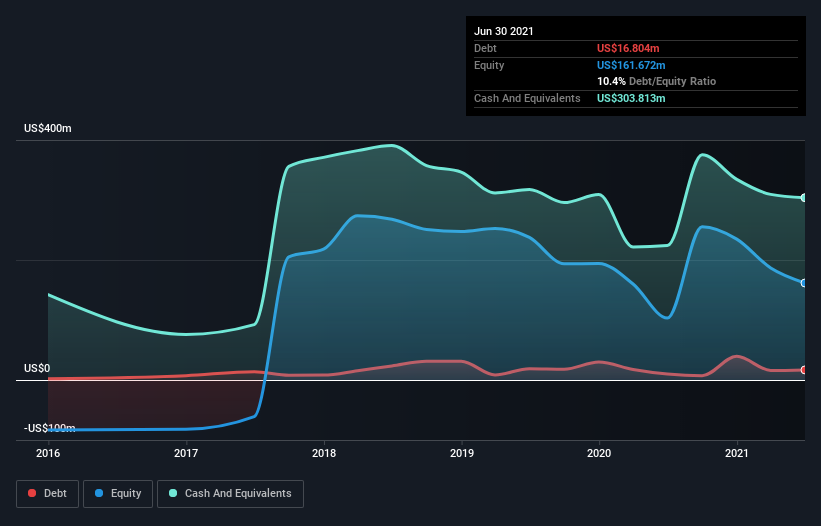

What Is Despegar.com’s Net Debt?

The image below, which you can click on for greater detail, shows that at June 2021 Despegar.com had debt of US$16.8m, up from US$9.96m in one year. But on the other hand it also has US$303.8m in cash, leading to a US$287.0m net cash position.

A Look At Despegar.com’s Liabilities

The latest balance sheet data shows that Despegar.com had liabilities of US$395.8m due within a year, and liabilities of US$229.2m falling due after that. On the other hand, it had cash of US$303.8m and US$78.8m worth of receivables due within a year. So it has liabilities totalling US$242.4m more than its cash and near-term receivables, combined.

Despegar.com has a market capitalization of US$798.7m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. While it does have liabilities worth noting, Despegar.com also has more cash than debt, so we’re pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Despegar.com can strengthen its balance sheet over time.

Over 12 months, Despegar.com made a loss at the EBIT level, and saw its revenue drop to US$180m, which is a fall of 48%. To be frank that doesn’t bode well.

So How Risky Is Despegar.com?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Despegar.com had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of US$93m and booked a US$146m accounting loss. Given it only has net cash of US$287.0m, the company may need to raise more capital if it doesn’t reach break-even soon. Overall, we’d say the stock is a bit risky, and we’re usually very cautious until we see positive free cash flow.