David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Delta Air Lines, Inc. (NYSE:DAL) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Delta Air Lines’s Debt?

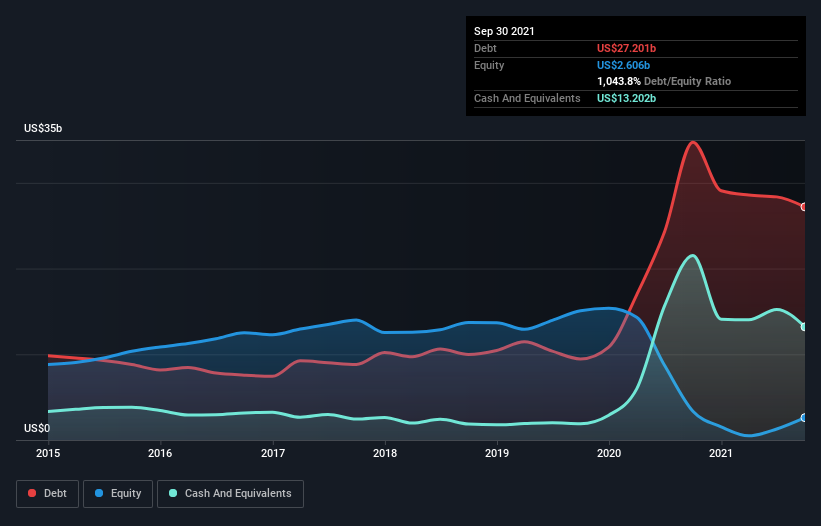

As you can see below, Delta Air Lines had US$27.2b of debt at September 2021, down from US$34.7b a year prior. However, it does have US$13.2b in cash offsetting this, leading to net debt of about US$14.0b.

How Healthy Is Delta Air Lines’ Balance Sheet?

The latest balance sheet data shows that Delta Air Lines had liabilities of US$20.9b due within a year, and liabilities of US$49.3b falling due after that. On the other hand, it had cash of US$13.2b and US$2.18b worth of receivables due within a year. So it has liabilities totalling US$54.8b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the US$25.1b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. After all, Delta Air Lines would likely require a major re-capitalisation if it had to pay its creditors today. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Delta Air Lines’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Delta Air Lines saw its revenue hold pretty steady, and it did not report positive earnings before interest and tax. While that’s not too bad, we’d prefer see growth.

Caveat Emptor

Importantly, Delta Air Lines had an earnings before interest and tax (EBIT) loss over the last year. Its EBIT loss was a whopping US$4.3b. Considering that alongside the liabilities mentioned above make us nervous about the company. We’d want to see some strong near-term improvements before getting too interested in the stock. Not least because it burned through US$1.2b in negative free cash flow over the last year. That means it’s on the risky side of things. The balance sheet is clearly the area to focus on when you are analysing debt.