David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Delcath Systems, Inc. (NASDAQ:DCTH) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Delcath Systems’s Net Debt?

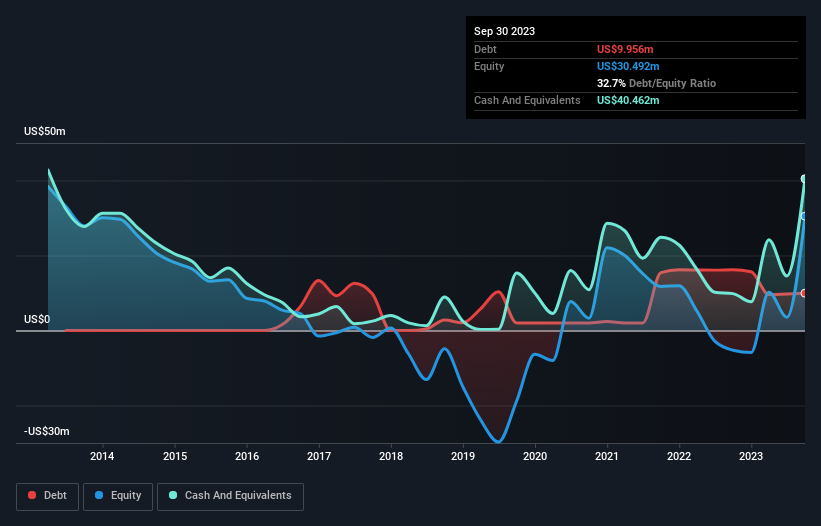

You can click the graphic below for the historical numbers, but it shows that Delcath Systems had US$9.96m of debt in September 2023, down from US$16.2m, one year before. However, it does have US$40.5m in cash offsetting this, leading to net cash of US$30.5m.

A Look At Delcath Systems’ Liabilities

The latest balance sheet data shows that Delcath Systems had liabilities of US$14.0m due within a year, and liabilities of US$3.11m falling due after that. Offsetting this, it had US$40.5m in cash and US$205.0k in receivables that were due within 12 months. So it actually has US$23.6m more liquid assets than total liabilities.

This surplus suggests that Delcath Systems is using debt in a way that is appears to be both safe and conservative. Given it has easily adequate short term liquidity, we don’t think it will have any issues with its lenders. Succinctly put, Delcath Systems boasts net cash, so it’s fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Delcath Systems can strengthen its balance sheet over time.

Over 12 months, Delcath Systems made a loss at the EBIT level, and saw its revenue drop to US$2.2m, which is a fall of 48%. That makes us nervous, to say the least.

So How Risky Is Delcath Systems?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Delcath Systems had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through US$30m of cash and made a loss of US$45m. But at least it has US$30.5m on the balance sheet to spend on growth, near-term. Overall, its balance sheet doesn’t seem overly risky, at the moment, but we’re always cautious until we see the positive free cash flow.