Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies CTS Corporation (NYSE:CTS) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is CTS’s Debt?

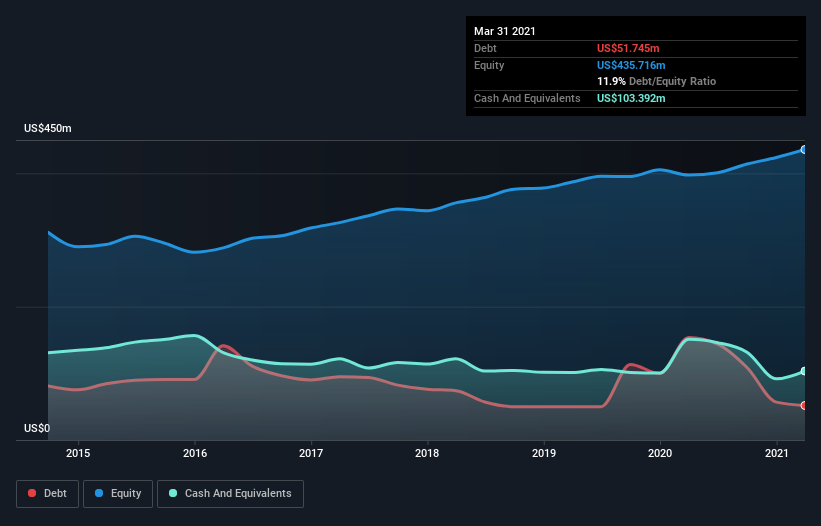

As you can see below, CTS had US$51.7m of debt at March 2021, down from US$153.6m a year prior. But on the other hand it also has US$103.4m in cash, leading to a US$51.6m net cash position.

How Strong Is CTS’ Balance Sheet?

The latest balance sheet data shows that CTS had liabilities of US$106.7m due within a year, and liabilities of US$92.2m falling due after that. On the other hand, it had cash of US$103.4m and US$81.6m worth of receivables due within a year. So its liabilities total US$14.0m more than the combination of its cash and short-term receivables.

Having regard to CTS’ size, it seems that its liquid assets are well balanced with its total liabilities. So while it’s hard to imagine that the US$1.09b company is struggling for cash, we still think it’s worth monitoring its balance sheet. While it does have liabilities worth noting, CTS also has more cash than debt, so we’re pretty confident it can manage its debt safely.

Fortunately, CTS grew its EBIT by 3.1% in the last year, making that debt load look even more manageable. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine CTS’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While CTS has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, CTS recorded free cash flow worth a fulsome 80% of its EBIT, which is stronger than we’d usually expect. That positions it well to pay down debt if desirable to do so.

Summing up

We could understand if investors are concerned about CTS’s liabilities, but we can be reassured by the fact it has has net cash of US$51.6m. And it impressed us with free cash flow of US$73m, being 80% of its EBIT. So is CTS’s debt a risk? It doesn’t seem so to us.