Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Colfax Corporation (NYSE:CFX) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

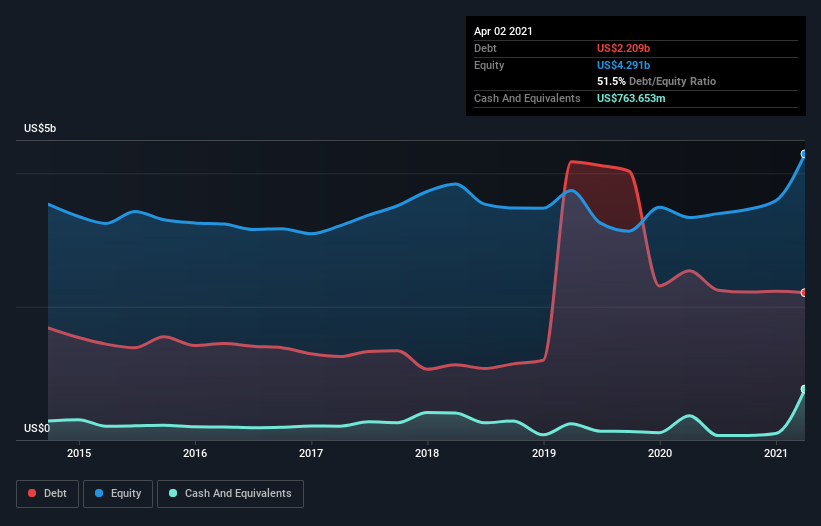

How Much Debt Does Colfax Carry?

As you can see below, Colfax had US$2.21b of debt at April 2021, down from US$2.54b a year prior. However, it does have US$763.7m in cash offsetting this, leading to net debt of about US$1.45b.

How Healthy Is Colfax’s Balance Sheet?

We can see from the most recent balance sheet that Colfax had liabilities of US$1.56b falling due within a year, and liabilities of US$2.22b due beyond that. Offsetting these obligations, it had cash of US$763.7m as well as receivables valued at US$553.8m due within 12 months. So its liabilities total US$2.46b more than the combination of its cash and short-term receivables.

Colfax has a market capitalization of US$6.11b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While Colfax’s debt to EBITDA ratio (3.1) suggests that it uses some debt, its interest cover is very weak, at 2.0, suggesting high leverage. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. Worse, Colfax’s EBIT was down 32% over the last year. If earnings keep going like that over the long term, it has a snowball’s chance in hell of paying off that debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Colfax’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, Colfax recorded free cash flow worth 55% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

To be frank both Colfax’s interest cover and its track record of (not) growing its EBIT make us rather uncomfortable with its debt levels. But at least it’s pretty decent at converting EBIT to free cash flow; that’s encouraging. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Colfax stock a bit risky. That’s not necessarily a bad thing, but we’d generally feel more comfortable with less leverage. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.