Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that CACI International Inc (NYSE:CACI) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

What Is CACI International’s Debt?

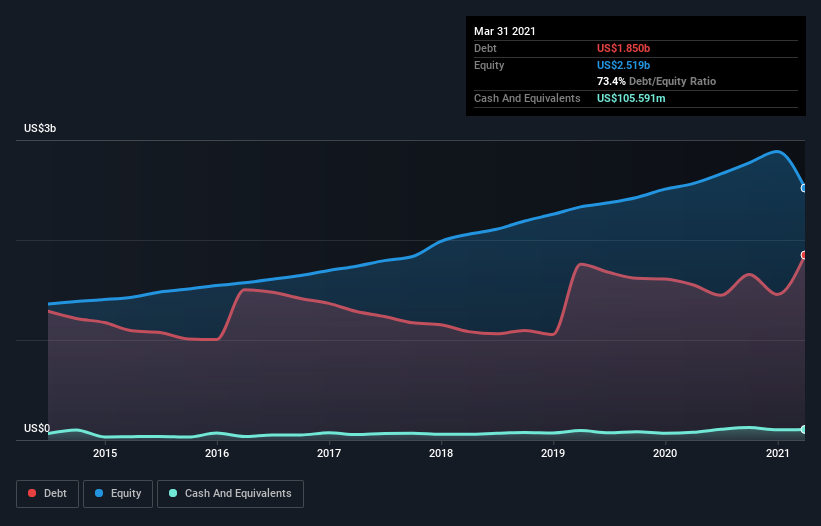

You can click the graphic below for the historical numbers, but it shows that as of March 2021 CACI International had US$1.85b of debt, an increase on US$1.55b, over one year. However, it does have US$105.6m in cash offsetting this, leading to net debt of about US$1.74b.

How Healthy Is CACI International’s Balance Sheet?

According to the last reported balance sheet, CACI International had liabilities of US$842.9m due within 12 months, and liabilities of US$2.61b due beyond 12 months. Offsetting this, it had US$105.6m in cash and US$860.7m in receivables that were due within 12 months. So it has liabilities totalling US$2.48b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since CACI International has a market capitalization of US$6.00b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

CACI International has a debt to EBITDA ratio of 2.5, which signals significant debt, but is still pretty reasonable for most types of business. But its EBIT was about 14.7 times its interest expense, implying the company isn’t really paying a high cost to maintain that level of debt. Even were the low cost to prove unsustainable, that is a good sign. Importantly, CACI International grew its EBIT by 35% over the last twelve months, and that growth will make it easier to handle its debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if CACI International can strengthen its balance sheet over time. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, CACI International actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Happily, CACI International’s impressive interest cover implies it has the upper hand on its debt. But, on a more sombre note, we are a little concerned by its net debt to EBITDA. Zooming out, CACI International seems to use debt quite reasonably; and that gets the nod from us. After all, sensible leverage can boost returns on equity. There’s no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet.