Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Boston Scientific Corporation (NYSE:BSX) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Boston Scientific Carry?

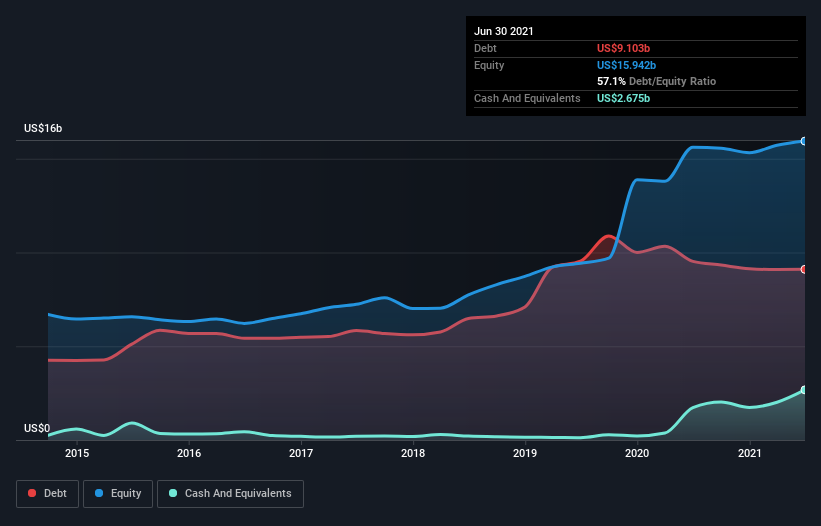

The image below, which you can click on for greater detail, shows that Boston Scientific had debt of US$9.10b at the end of June 2021, a reduction from US$9.53b over a year. On the flip side, it has US$2.68b in cash leading to net debt of about US$6.43b.

How Strong Is Boston Scientific’s Balance Sheet?

The latest balance sheet data shows that Boston Scientific had liabilities of US$4.07b due within a year, and liabilities of US$11.2b falling due after that. Offsetting these obligations, it had cash of US$2.68b as well as receivables valued at US$1.68b due within 12 months. So it has liabilities totalling US$10.9b more than its cash and near-term receivables, combined.

Given Boston Scientific has a humongous market capitalization of US$62.2b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Boston Scientific has net debt worth 2.2 times EBITDA, which isn’t too much, but its interest cover looks a bit on the low side, with EBIT at only 5.2 times the interest expense. While that doesn’t worry us too much, it does suggest the interest payments are somewhat of a burden. Importantly, Boston Scientific grew its EBIT by 59% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Boston Scientific’s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Boston Scientific recorded free cash flow worth a fulsome 80% of its EBIT, which is stronger than we’d usually expect. That positions it well to pay down debt if desirable to do so.

Our View

Happily, Boston Scientific’s impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. And that’s just the beginning of the good news since its EBIT growth rate is also very heartening. It’s also worth noting that Boston Scientific is in the Medical Equipment industry, which is often considered to be quite defensive. Zooming out, Boston Scientific seems to use debt quite reasonably; and that gets the nod from us. While debt does bring risk, when used wisely it can also bring a higher return on equity.