Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Bloom Energy Corporation (NYSE:BE) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Bloom Energy Carry?

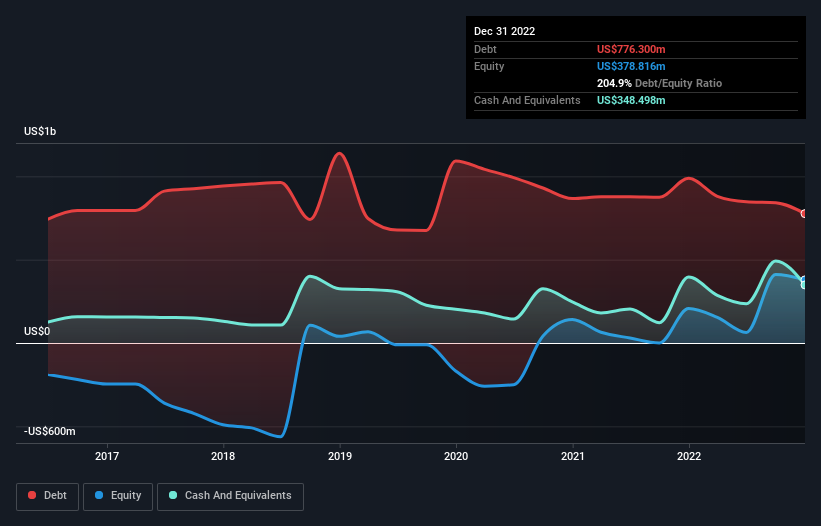

The image below, which you can click on for greater detail, shows that Bloom Energy had debt of US$776.3m at the end of December 2022, a reduction from US$988.6m over a year. However, it also had US$348.5m in cash, and so its net debt is US$427.8m.

How Strong Is Bloom Energy’s Balance Sheet?

We can see from the most recent balance sheet that Bloom Energy had liabilities of US$541.9m falling due within a year, and liabilities of US$1.03b due beyond that. On the other hand, it had cash of US$348.5m and US$308.0m worth of receivables due within a year. So its liabilities total US$911.4m more than the combination of its cash and short-term receivables.

Bloom Energy has a market capitalization of US$3.36b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Bloom Energy can strengthen its balance sheet over time.

Over 12 months, Bloom Energy reported revenue of US$1.2b, which is a gain of 23%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

Caveat Emptor

While we can certainly appreciate Bloom Energy’s revenue growth, its earnings before interest and tax (EBIT) loss is not ideal. To be specific the EBIT loss came in at US$152m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. However, it doesn’t help that it burned through US$309m of cash over the last year. So in short it’s a really risky stock. There’s no doubt that we learn most about debt from the balance sheet.