David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies BlackLine, Inc. (NASDAQ:BL) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is BlackLine’s Debt?

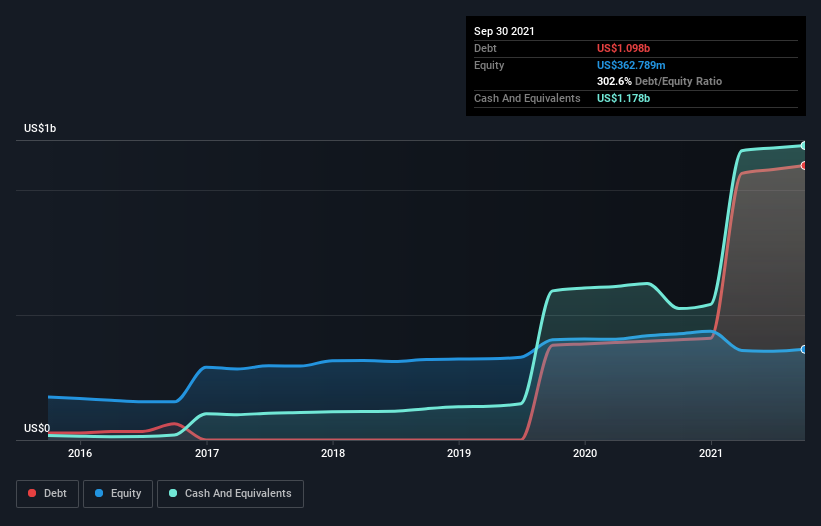

The image below, which you can click on for greater detail, shows that at September 2021 BlackLine had debt of US$1.10b, up from US$401.2m in one year. But on the other hand it also has US$1.18b in cash, leading to a US$80.0m net cash position.

How Strong Is BlackLine’s Balance Sheet?

According to the last reported balance sheet, BlackLine had liabilities of US$256.2m due within 12 months, and liabilities of US$1.13b due beyond 12 months. Offsetting these obligations, it had cash of US$1.18b as well as receivables valued at US$105.0m due within 12 months. So its liabilities total US$104.6m more than the combination of its cash and short-term receivables.

Given BlackLine has a market capitalization of US$5.22b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, BlackLine also has more cash than debt, so we’re pretty confident it can manage its debt safely. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine BlackLine’s ability to maintain a healthy balance sheet going forward.

Over 12 months, BlackLine reported revenue of US$406m, which is a gain of 21%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is BlackLine?

While BlackLine lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow US$50m. So taking that on face value, and considering the net cash situation, we don’t think that the stock is too risky in the near term. One positive is that BlackLine is growing revenue apace, which makes it easier to sell a growth story and raise capital if need be. But we still think it’s somewhat risky.