Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Axsome Therapeutics, Inc. (NASDAQ:AXSM) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Axsome Therapeutics Carry?

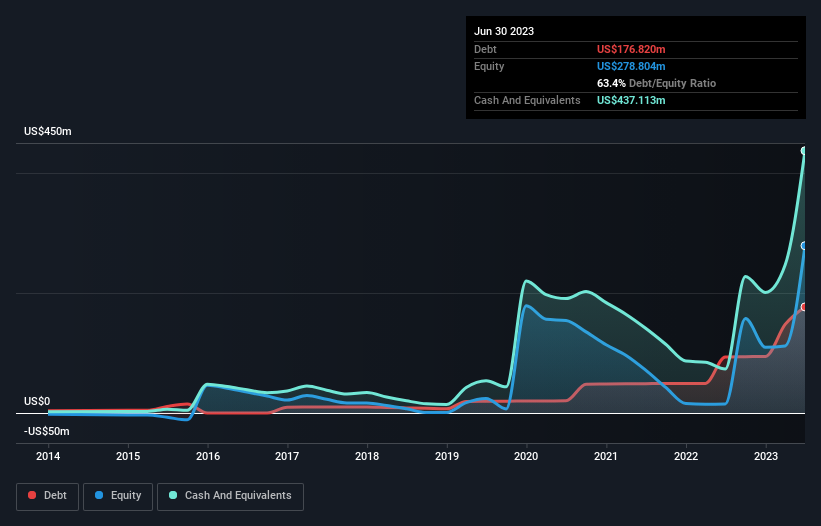

The image below, which you can click on for greater detail, shows that at June 2023 Axsome Therapeutics had debt of US$176.8m, up from US$93.5m in one year. But it also has US$437.1m in cash to offset that, meaning it has US$260.3m net cash.

A Look At Axsome Therapeutics’ Liabilities

Zooming in on the latest balance sheet data, we can see that Axsome Therapeutics had liabilities of US$115.0m due within 12 months and liabilities of US$217.9m due beyond that. Offsetting this, it had US$437.1m in cash and US$67.4m in receivables that were due within 12 months. So it can boast US$171.7m more liquid assets than total liabilities.

This surplus suggests that Axsome Therapeutics has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Axsome Therapeutics has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Axsome Therapeutics can strengthen its balance sheet over time.

In the last year Axsome Therapeutics wasn’t profitable at an EBIT level, but managed to grow its revenue by 1,969%, to US$182m. That’s virtually the hole-in-one of revenue growth!

So How Risky Is Axsome Therapeutics?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months Axsome Therapeutics lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$112m and booked a US$184m accounting loss. While this does make the company a bit risky, it’s important to remember it has net cash of US$260.3m. That means it could keep spending at its current rate for more than two years. Importantly, Axsome Therapeutics’s revenue growth is hot to trot. While unprofitable companies can be risky, they can also grow hard and fast in those pre-profit years.