Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Aspen Aerogels, Inc. (NYSE:ASPN) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Aspen Aerogels’s Net Debt?

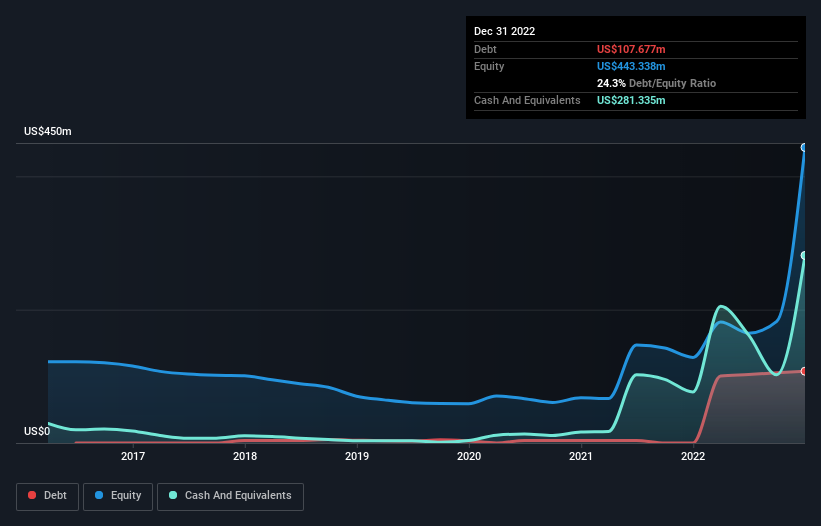

You can click the graphic below for the historical numbers, but it shows that as of December 2022 Aspen Aerogels had US$107.7m of debt, an increase on none, over one year. However, its balance sheet shows it holds US$281.3m in cash, so it actually has US$173.7m net cash.

How Strong Is Aspen Aerogels’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Aspen Aerogels had liabilities of US$79.3m due within 12 months and liabilities of US$123.9m due beyond that. Offsetting this, it had US$281.3m in cash and US$57.4m in receivables that were due within 12 months. So it can boast US$135.5m more liquid assets than total liabilities.

This excess liquidity suggests that Aspen Aerogels is taking a careful approach to debt. Due to its strong net asset position, it is not likely to face issues with its lenders. Simply put, the fact that Aspen Aerogels has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Aspen Aerogels can strengthen its balance sheet over time.

In the last year Aspen Aerogels wasn’t profitable at an EBIT level, but managed to grow its revenue by 48%, to US$180m. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Aspen Aerogels?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Aspen Aerogels lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$209m and booked a US$83m accounting loss. While this does make the company a bit risky, it’s important to remember it has net cash of US$173.7m. That means it could keep spending at its current rate for more than two years. Aspen Aerogels’s revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course. By investing before those profits, shareholders take on more risk in the hope of bigger rewards.