David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that AptarGroup, Inc. (NYSE:ATR) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

What Is AptarGroup’s Debt?

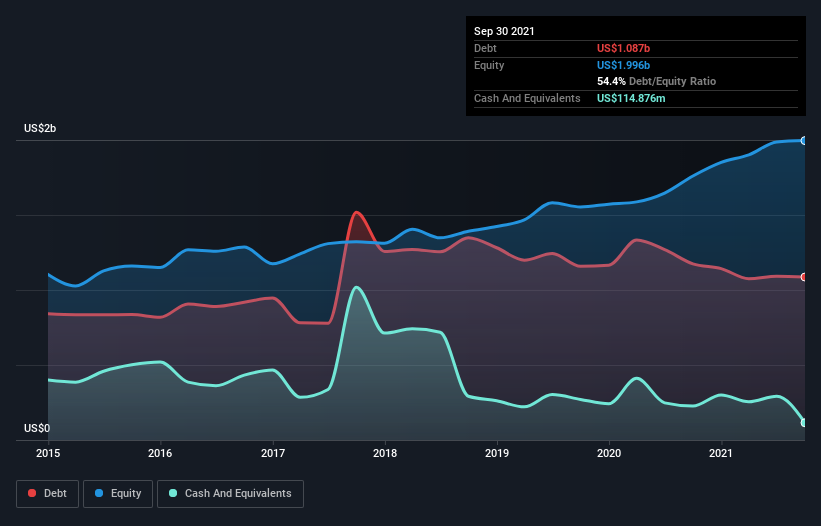

You can click the graphic below for the historical numbers, but it shows that AptarGroup had US$1.09b of debt in September 2021, down from US$1.17b, one year before. However, it also had US$114.9m in cash, and so its net debt is US$971.7m.

How Healthy Is AptarGroup’s Balance Sheet?

We can see from the most recent balance sheet that AptarGroup had liabilities of US$908.4m falling due within a year, and liabilities of US$1.23b due beyond that. Offsetting these obligations, it had cash of US$114.9m as well as receivables valued at US$680.8m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$1.34b.

Given AptarGroup has a market capitalization of US$7.66b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

We’d say that AptarGroup’s moderate net debt to EBITDA ratio ( being 1.6), indicates prudence when it comes to debt. And its strong interest cover of 17.0 times, makes us even more comfortable. The good news is that AptarGroup has increased its EBIT by 3.3% over twelve months, which should ease any concerns about debt repayment. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if AptarGroup can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, AptarGroup produced sturdy free cash flow equating to 59% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

AptarGroup’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And its conversion of EBIT to free cash flow is good too. Looking at all the aforementioned factors together, it strikes us that AptarGroup can handle its debt fairly comfortably. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it’s worth monitoring the balance sheet.