Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Appian Corporation (NASDAQ:APPN) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Appian’s Debt?

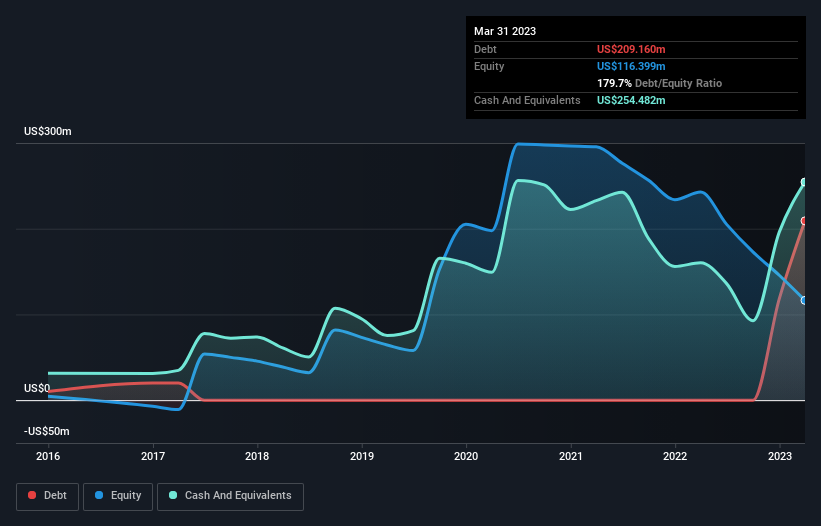

As you can see below, at the end of March 2023, Appian had US$209.2m of debt, up from none a year ago. Click the image for more detail. But on the other hand it also has US$254.5m in cash, leading to a US$45.3m net cash position.

How Strong Is Appian’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Appian had liabilities of US$323.8m due within 12 months and liabilities of US$204.7m due beyond that. Offsetting this, it had US$254.5m in cash and US$147.6m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$126.4m.

Since publicly traded Appian shares are worth a total of US$3.84b, it seems unlikely that this level of liabilities would be a major threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, Appian also has more cash than debt, so we’re pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Appian can strengthen its balance sheet over time.

In the last year Appian wasn’t profitable at an EBIT level, but managed to grow its revenue by 24%, to US$489m. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Appian?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that Appian had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through US$121m of cash and made a loss of US$165m. But the saving grace is the US$45.3m on the balance sheet. That kitty means the company can keep spending for growth for at least two years, at current rates. With very solid revenue growth in the last year, Appian may be on a path to profitability. Pre-profit companies are often risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start.