Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Adaptive Biotechnologies Corporation (NASDAQ:ADPT) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Adaptive Biotechnologies’s Net Debt?

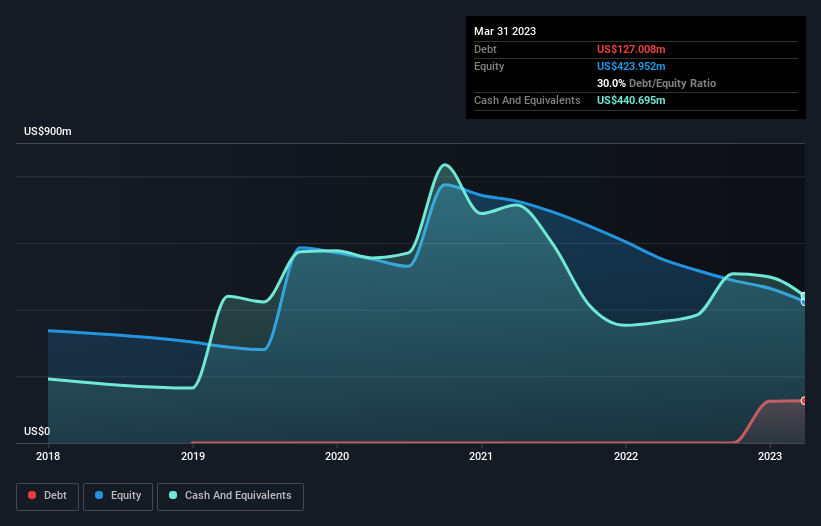

You can click the graphic below for the historical numbers, but it shows that as of March 2023 Adaptive Biotechnologies had US$127.0m of debt, an increase on none, over one year. However, its balance sheet shows it holds US$440.7m in cash, so it actually has US$313.7m net cash.

A Look At Adaptive Biotechnologies’ Liabilities

Zooming in on the latest balance sheet data, we can see that Adaptive Biotechnologies had liabilities of US$90.1m due within 12 months and liabilities of US$277.4m due beyond that. Offsetting this, it had US$440.7m in cash and US$31.9m in receivables that were due within 12 months. So it can boast US$105.1m more liquid assets than total liabilities.

This surplus suggests that Adaptive Biotechnologies has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Adaptive Biotechnologies has more cash than debt is arguably a good indication that it can manage its debt safely. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Adaptive Biotechnologies’s ability to maintain a healthy balance sheet going forward.

In the last year Adaptive Biotechnologies wasn’t profitable at an EBIT level, but managed to grow its revenue by 19%, to US$184m. We usually like to see faster growth from unprofitable companies, but each to their own.

So How Risky Is Adaptive Biotechnologies?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that Adaptive Biotechnologies had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through US$195m of cash and made a loss of US$195m. While this does make the company a bit risky, it’s important to remember it has net cash of US$313.7m. That means it could keep spending at its current rate for more than two years. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn’t produce free cash flow regularly. The balance sheet is clearly the area to focus on when you are analysing debt.