Summary

- The company is involved in several businesses including telecoms, electric vehicles, and debit card payments.

- Revenues are growing rapidly and iQSTEL expects its new debit card service to generate revenues of $45-$128 million over a five-year period with an EBITDA margin of 30%-40%.

- However, iQSTEL is currently unprofitable and its shareholders’ equity position was negative as of September 2020.

- It seems the company is popular on social media platforms and there could be a significant retail investor interest at the moment.

- I don’t think the business is worth much in this current state.

Investment thesis

iQSTEL (OTCPK:IQST) is telecommunications company linked with a significant number of sectors that are currently popular with retail investors, including Internet of things, electric vehicles, fintech, and blockchain.

It recently announced the launch a Visa prepaid debit card service, which it expects to generate revenues of $45-$128 million over a five-year period with an EBITDA margin of 30%-40%.

However, I think that the company is a sell as its margins are terrible, its balance sheet is weak; and I doubt the Visa prepaid debit card service can generate meaningful revenues. Also, its soaring valuation seems to be fueled by promotion on social media platforms.

Overview of the business

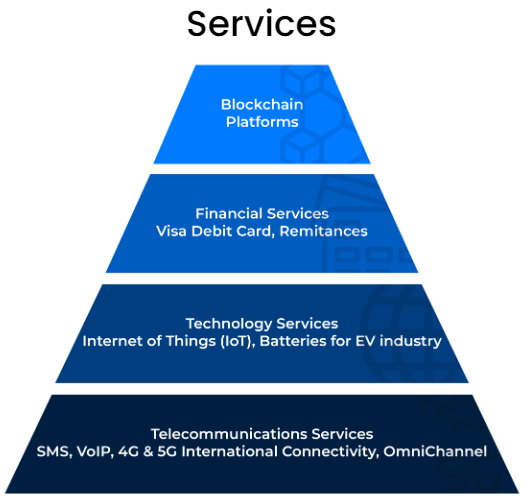

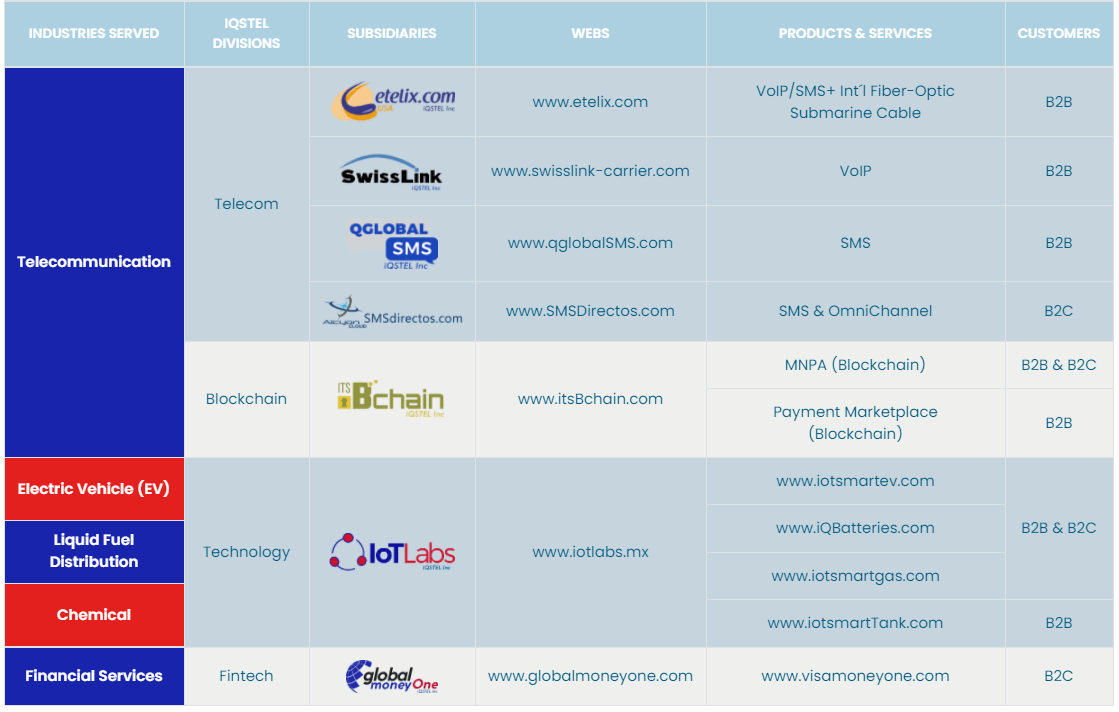

iQSTEL has a total of seven subsidiaries spread across four business divisions, namely telecom, technology, fintech, and blockchain. Its product portfolio includes VoIP, 4G and 5G international infrastructure connectivity, IoT Smart EV, debit card, and blockchain payment marketplace solutions among other.

(Source: iQSTEL)

In February, its wholesale SMS termination arm QGlobal SMS inked a partnership agreement with cloud communications provider Vonage (NASDAQ:VG).

Regarding the new Visa prepaid debit card service that I mentioned, iQSTEL will own a 75% in through Global Money One. The other 25% in the latter is owned by Payment Virtual Mobile Solutions (PayVMS).

The company recently announced plans to develop a proprietary electric battery after it entered in a partnership with Modus Group. The latter is working on the Revolt electric motorcycle of Alternet Systems (OTC:OTCPK:ALYI).

iQSTEL has operations in a total of 13 countries and expects to generate revenues of $60.5 million in 2021. It has a rapidly growing business, considering 2019 and 2020 revenues came in at $19 million and $44.8 million, respectively.

The company is currently pursuing a listing on NASDAQ and recently became debt-free following the elimination of $3.3 million of debt in the last quarter of 2020.

Financials and valuation

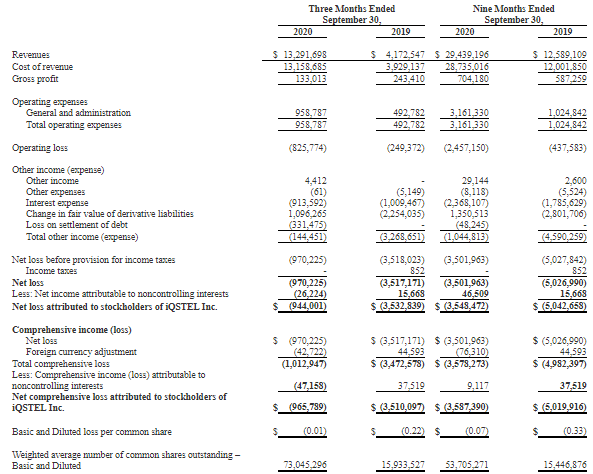

While the business is growing fast, the margins are worsening and iQSTEL is bleeding money.

The latest available financials are for Q3 2020. In the first nine months of 2020, the company booked an operating loss of $$2.46 million and the net cash from operating activities came in at negative $1.53 million.

(Source: SEC)

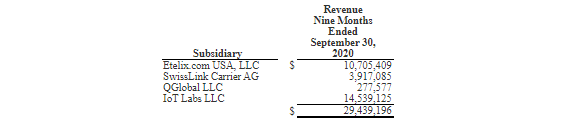

iQSTEL is involved in many businesses, but the bulk of its revenues come from its telecommunications and technology divisions.

(Source: SEC)

Etelix provides international and domestic long-distance voice termination solutions in the ILD wholesale market. IoT Labs is focused on the sale of SMS between USA and Mexico and was bought in April 2020. The pro-forma Q3 2020 results indicate that this is iQSTEL’s main subsidiary.

(Source: SEC)

iQSTEL has an asset-light business model and its total assets stood at just $5.32 million as of September 2020. Intangible assets, goodwill and deferred taxes accounted for more than $2 million of them.

As of September, the shareholders’ equity was negative and the company had negative working capital, which I think is a significant red flag.

(Source: SEC)

Looking at 2021, iQSTEL expects to book revenues of $60.5 million, with the telecommunications division accounting for $55.1 million of them.

This means that the Visa prepaid debit card service (in the fintech division) is unlikely to generate significant revenues this year. Considering the company barely has any funds, I doubt it can promote this business and grow it to $25 million in revenues per year. The new service is expected to be launched by June 2020.

According to OTC Markets, iQSTEL currently has 129,314,064 shares outstanding and its market capitalization stands at $148.6 million as of March 12.

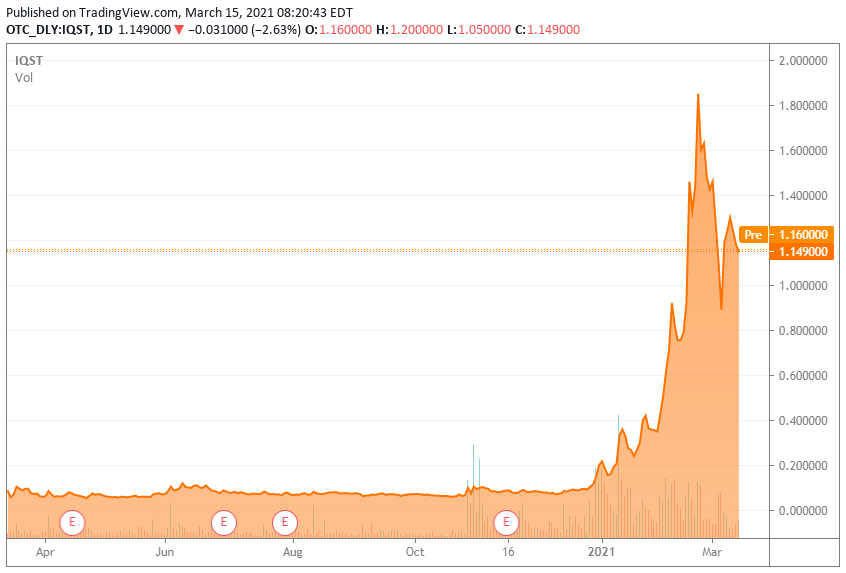

The company’s share price started soaring around the end of December and I think a significant reason for its recent popularity among retail investors could be due to social media promotion.

(Source: TradingView)

iQSTEL and social media

The company is currently popular on platforms such as twitter and Stockwits. Every few minutes, there’s a new tweet with the $IQST hashtag.

On YouTube, iQSTEL is covered by several channels such as Mike Jones Investing, Stockzilla, Soulstring Media, Money Core, and Daniel Vill. It seems that more frequent posting of videos on the company started around the start of February. Several of the videos of Mike Jones Investing have attracted over 10k views, so I think that retail investor interest in iQSTEL could be somewhat significant.

The company’s own subreddit was created on February 17, but it hasn’t picked up steam yet. It has just 136 members as of time of writing.

Investor takeaway

iQSTEL is a relatively small and unprofitable telecommunications company, which seems to be currently popular with retails investors due to its ties to several trendy sectors like EV and blockchain. I think this is to a large extent due to promotion on social media platforms like twitter.

In my opinion, iQSTEL is a in a bad situation from a fundamentals point of view and is a sell. Investors can take advantage of this by shorting the shares. According to data from Fintel, the short borrow fee rate currently stands at 3.50%.

There are two major risks I see for the bear thesis. First, it’s possible that I’m wrong about the potential of the company’s debit card product and the latter turns iQSTEL into a profitable company. Second, the share price of the iQSTEL could soar again due to higher retail investor interest as a result of the listing on NASDAQ.