David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that HireQuest, Inc. (NASDAQ:HQI) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

What Is HireQuest’s Net Debt?

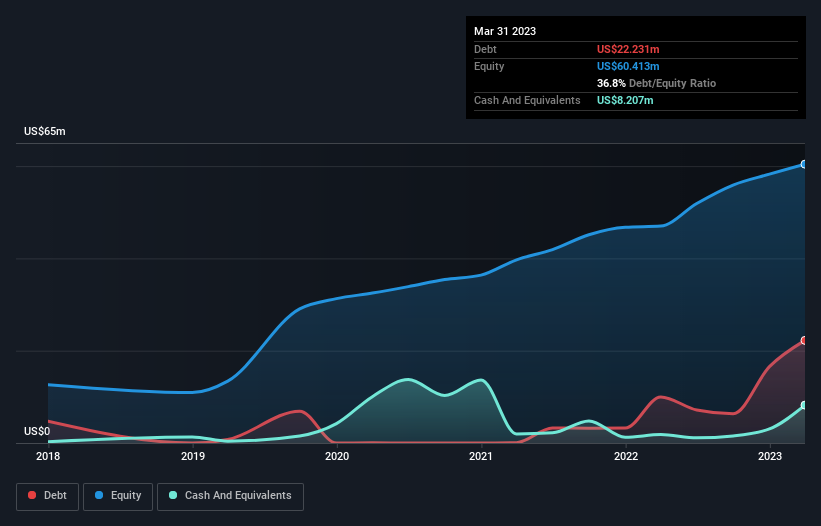

You can click the graphic below for the historical numbers, but it shows that as of March 2023 HireQuest had US$22.2m of debt, an increase on US$9.98m, over one year. However, it does have US$8.21m in cash offsetting this, leading to net debt of about US$14.0m.

How Healthy Is HireQuest’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that HireQuest had liabilities of US$44.9m due within 12 months and liabilities of US$5.25m due beyond that. On the other hand, it had cash of US$8.21m and US$49.1m worth of receivables due within a year. So it actually has US$7.15m more liquid assets than total liabilities.

This surplus suggests that HireQuest has a conservative balance sheet, and could probably eliminate its debt without much difficulty.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

HireQuest’s net debt is only 0.78 times its EBITDA. And its EBIT covers its interest expense a whopping 23.9 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Also positive, HireQuest grew its EBIT by 28% in the last year, and that should make it easier to pay down debt, going forward. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if HireQuest can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Happily for any shareholders, HireQuest actually produced more free cash flow than EBIT over the last three years. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Our View

Happily, HireQuest’s impressive interest cover implies it has the upper hand on its debt. And that’s just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. We think HireQuest is no more beholden to its lenders, than the birds are to birdwatchers. For investing nerds like us its balance sheet is almost charming. The balance sheet is clearly the area to focus on when you are analysing debt.