Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that W.W. Grainger, Inc. (NYSE:GWW) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

What Is W.W. Grainger’s Net Debt?

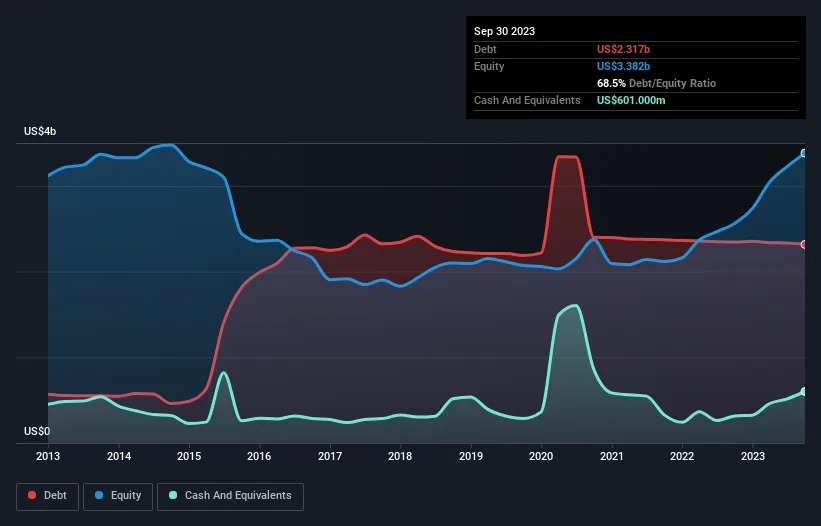

The chart below, which you can click on for greater detail, shows that W.W. Grainger had US$2.32b in debt in September 2023; about the same as the year before. However, it also had US$601.0m in cash, and so its net debt is US$1.72b.

How Healthy Is W.W. Grainger’s Balance Sheet?

The latest balance sheet data shows that W.W. Grainger had liabilities of US$1.90b due within a year, and liabilities of US$2.86b falling due after that. Offsetting this, it had US$601.0m in cash and US$2.44b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$1.71b.

Given W.W. Grainger has a humongous market capitalization of US$41.1b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

W.W. Grainger’s net debt is only 0.62 times its EBITDA. And its EBIT covers its interest expense a whopping 27.5 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. And we also note warmly that W.W. Grainger grew its EBIT by 13% last year, making its debt load easier to handle. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine W.W. Grainger’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, W.W. Grainger produced sturdy free cash flow equating to 51% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

The good news is that W.W. Grainger’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And that’s just the beginning of the good news since its net debt to EBITDA is also very heartening. Looking at the bigger picture, we think W.W. Grainger’s use of debt seems quite reasonable and we’re not concerned about it. After all, sensible leverage can boost returns on equity. The balance sheet is clearly the area to focus on when you are analysing debt.