Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that SkyWest, Inc. (NASDAQ:SKYW) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is SkyWest’s Net Debt?

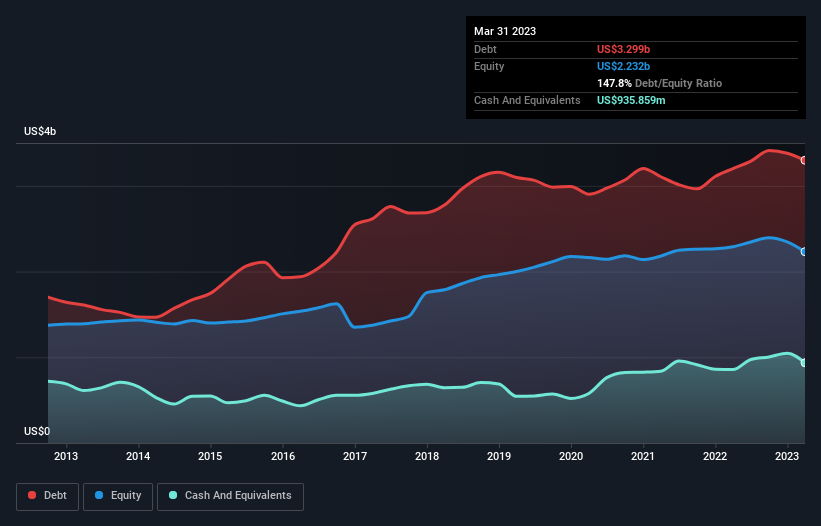

The chart below, which you can click on for greater detail, shows that SkyWest had US$3.30b in debt in March 2023; about the same as the year before. However, it does have US$935.9m in cash offsetting this, leading to net debt of about US$2.36b.

A Look At SkyWest’s Liabilities

We can see from the most recent balance sheet that SkyWest had liabilities of US$1.15b falling due within a year, and liabilities of US$3.85b due beyond that. Offsetting this, it had US$935.9m in cash and US$101.0m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$3.96b.

This deficit casts a shadow over the US$1.82b company, like a colossus towering over mere mortals. So we’d watch its balance sheet closely, without a doubt. At the end of the day, SkyWest would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While we wouldn’t worry about SkyWest’s net debt to EBITDA ratio of 4.6, we think its super-low interest cover of 1.2 times is a sign of high leverage. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. On a lighter note, we note that SkyWest grew its EBIT by 22% in the last year. If sustained, this growth should make that debt evaporate like a scarce drinking water during an unnaturally hot summer. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if SkyWest can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last two years, SkyWest burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

To be frank both SkyWest’s conversion of EBIT to free cash flow and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But at least it’s pretty decent at growing its EBIT; that’s encouraging. Taking into account all the aforementioned factors, it looks like SkyWest has too much debt. That sort of riskiness is ok for some, but it certainly doesn’t float our boat. When analysing debt levels, the balance sheet is the obvious place to start.