David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Roxgold Inc. (TSE:ROXG) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Roxgold’s Net Debt?

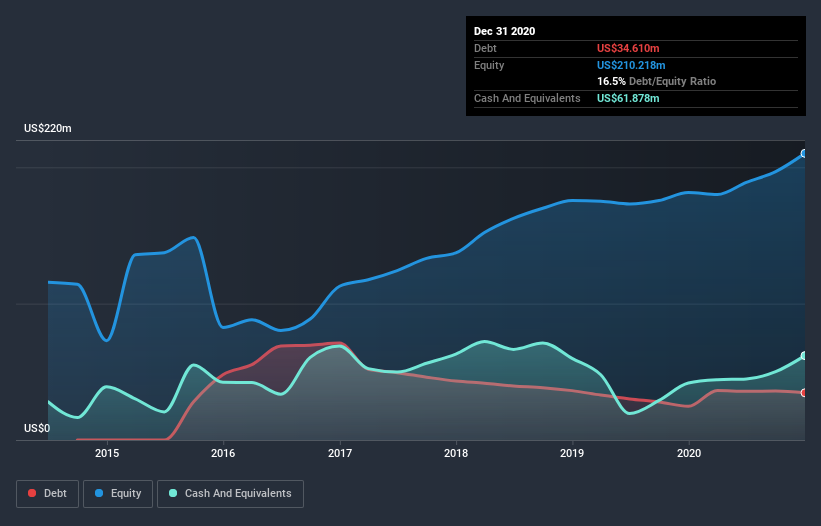

The image below, which you can click on for greater detail, shows that at December 2020 Roxgold had debt of US$34.6m, up from US$24.7m in one year. But on the other hand it also has US$61.9m in cash, leading to a US$27.3m net cash position.

A Look At Roxgold’s Liabilities

The latest balance sheet data shows that Roxgold had liabilities of US$82.3m due within a year, and liabilities of US$51.0m falling due after that. Offsetting this, it had US$61.9m in cash and US$28.2m in receivables that were due within 12 months. So its liabilities total US$43.2m more than the combination of its cash and short-term receivables.

Of course, Roxgold has a market capitalization of US$608.0m, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, Roxgold boasts net cash, so it’s fair to say it does not have a heavy debt load!

In addition to that, we’re happy to report that Roxgold has boosted its EBIT by 58%, thus reducing the spectre of future debt repayments. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Roxgold can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. While Roxgold has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last three years, Roxgold created free cash flow amounting to 11% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Summing up

We could understand if investors are concerned about Roxgold’s liabilities, but we can be reassured by the fact it has has net cash of US$27.3m. And we liked the look of last year’s 58% year-on-year EBIT growth. So we don’t have any problem with Roxgold’s use of debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot.