David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that PENN Entertainment, Inc. (NASDAQ:PENN) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is PENN Entertainment’s Debt?

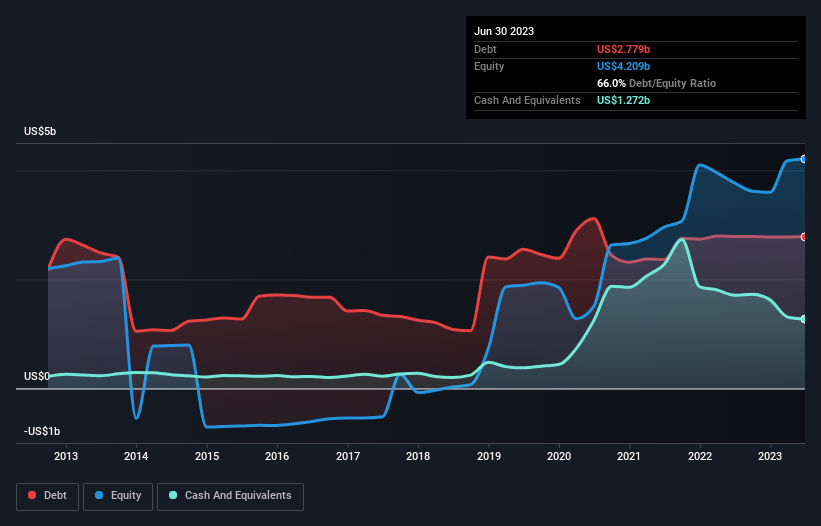

As you can see below, PENN Entertainment had US$2.78b of debt, at June 2023, which is about the same as the year before. You can click the chart for greater detail. On the flip side, it has US$1.27b in cash leading to net debt of about US$1.51b.

How Strong Is PENN Entertainment’s Balance Sheet?

We can see from the most recent balance sheet that PENN Entertainment had liabilities of US$1.23b falling due within a year, and liabilities of US$11.6b due beyond that. Offsetting this, it had US$1.27b in cash and US$289.6m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$11.3b.

This deficit casts a shadow over the US$3.42b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, PENN Entertainment would likely require a major re-capitalisation if it had to pay its creditors today.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

PENN Entertainment has a very low debt to EBITDA ratio of 1.0 so it is strange to see weak interest coverage, with last year’s EBIT being only 1.6 times the interest expense. So while we’re not necessarily alarmed we think that its debt is far from trivial. The bad news is that PENN Entertainment saw its EBIT decline by 15% over the last year. If earnings continue to decline at that rate then handling the debt will be more difficult than taking three children under 5 to a fancy pants restaurant. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if PENN Entertainment can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. During the last three years, PENN Entertainment produced sturdy free cash flow equating to 61% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

On the face of it, PENN Entertainment’s interest cover left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its net debt to EBITDA is a good sign, and makes us more optimistic. We’re quite clear that we consider PENN Entertainment to be really rather risky, as a result of its balance sheet health. So we’re almost as wary of this stock as a hungry kitten is about falling into its owner’s fish pond: once bitten, twice shy, as they say. There’s no doubt that we learn most about debt from the balance sheet.