The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Pegasystems Inc. (NASDAQ:PEGA) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Pegasystems’s Net Debt?

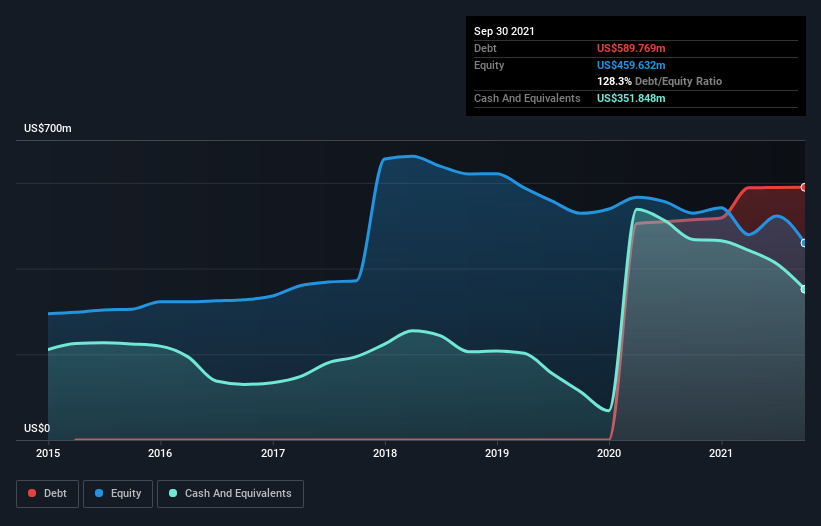

You can click the graphic below for the historical numbers, but it shows that as of September 2021 Pegasystems had US$589.8m of debt, an increase on US$513.8m, over one year. However, because it has a cash reserve of US$351.8m, its net debt is less, at about US$237.9m.

A Look At Pegasystems’ Liabilities

We can see from the most recent balance sheet that Pegasystems had liabilities of US$400.4m falling due within a year, and liabilities of US$695.3m due beyond that. On the other hand, it had cash of US$351.8m and US$394.7m worth of receivables due within a year. So it has liabilities totalling US$349.2m more than its cash and near-term receivables, combined.

Since publicly traded Pegasystems shares are worth a total of US$9.02b, it seems unlikely that this level of liabilities would be a major threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Pegasystems can strengthen its balance sheet over time.

In the last year Pegasystems wasn’t profitable at an EBIT level, but managed to grow its revenue by 20%, to US$1.2b. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Importantly, Pegasystems had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost US$68m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. For example, we would not want to see a repeat of last year’s loss of US$22m. So to be blunt we do think it is risky. There’s no doubt that we learn most about debt from the balance sheet.