The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Open Text Corporation (NASDAQ:OTEX) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Open Text’s Net Debt?

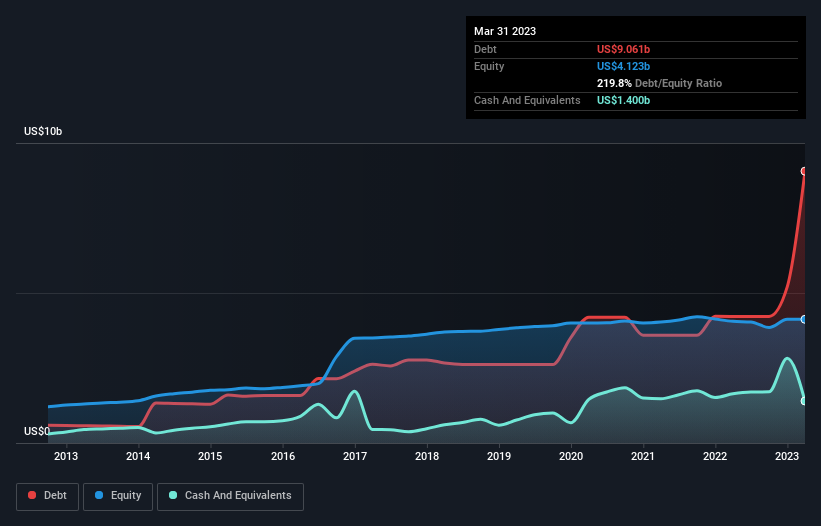

You can click the graphic below for the historical numbers, but it shows that as of March 2023 Open Text had US$9.06b of debt, an increase on US$4.22b, over one year. However, it also had US$1.40b in cash, and so its net debt is US$7.66b.

A Look At Open Text’s Liabilities

We can see from the most recent balance sheet that Open Text had liabilities of US$3.48b falling due within a year, and liabilities of US$9.82b due beyond that. Offsetting these obligations, it had cash of US$1.40b as well as receivables valued at US$785.5m due within 12 months. So it has liabilities totalling US$11.1b more than its cash and near-term receivables, combined.

This deficit is considerable relative to its very significant market capitalization of US$11.3b, so it does suggest shareholders should keep an eye on Open Text’s use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With a net debt to EBITDA ratio of 7.5, it’s fair to say Open Text does have a significant amount of debt. However, its interest coverage of 3.1 is reasonably strong, which is a good sign. More concerning, Open Text saw its EBIT drop by 6.2% in the last twelve months. If it keeps going like that paying off its debt will be like running on a treadmill — a lot of effort for not much advancement. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Open Text’s ability to maintain a healthy balance sheet going forward.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Happily for any shareholders, Open Text actually produced more free cash flow than EBIT over the last three years. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Our View

We’d go so far as to say Open Text’s net debt to EBITDA was disappointing. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Open Text stock a bit risky. That’s not necessarily a bad thing, but we’d generally feel more comfortable with less leverage. There’s no doubt that we learn most about debt from the balance sheet.