Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Construction Partners, Inc. (NASDAQ:ROAD) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Construction Partners’s Net Debt?

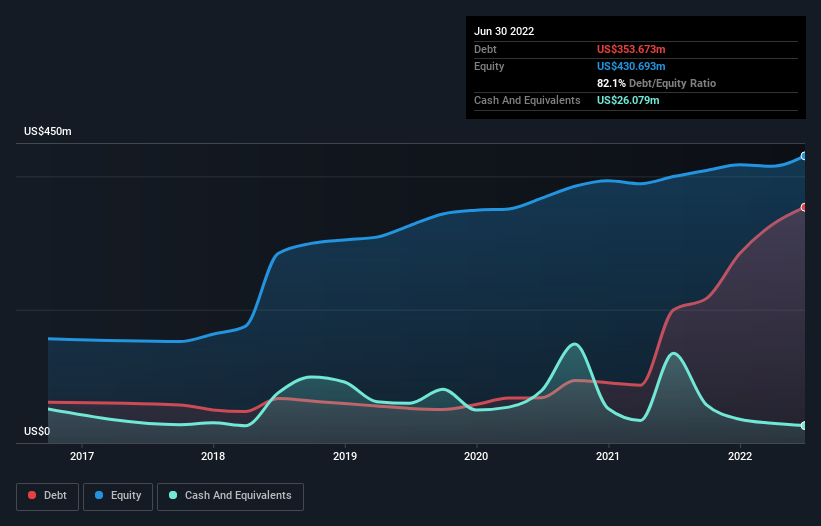

The image below, which you can click on for greater detail, shows that at June 2022 Construction Partners had debt of US$353.7m, up from US$199.5m in one year. However, it also had US$26.1m in cash, and so its net debt is US$327.6m.

How Healthy Is Construction Partners’ Balance Sheet?

According to the last reported balance sheet, Construction Partners had liabilities of US$204.1m due within 12 months, and liabilities of US$385.5m due beyond 12 months. On the other hand, it had cash of US$26.1m and US$272.8m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$290.7m.

Of course, Construction Partners has a market capitalization of US$1.68b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Construction Partners’s debt is 3.6 times its EBITDA, and its EBIT cover its interest expense 5.2 times over. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. Shareholders should be aware that Construction Partners’s EBIT was down 45% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Construction Partners can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Construction Partners reported free cash flow worth 7.3% of its EBIT, which is really quite low. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

Mulling over Construction Partners’s attempt at (not) growing its EBIT, we’re certainly not enthusiastic. Having said that, its ability to handle its total liabilities isn’t such a worry. Once we consider all the factors above, together, it seems to us that Construction Partners’s debt is making it a bit risky. Some people like that sort of risk, but we’re mindful of the potential pitfalls, so we’d probably prefer it carry less debt. There’s no doubt that we learn most about debt from the balance sheet.