Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that AdaptHealth Corp. (NASDAQ:AHCO) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is AdaptHealth’s Debt?

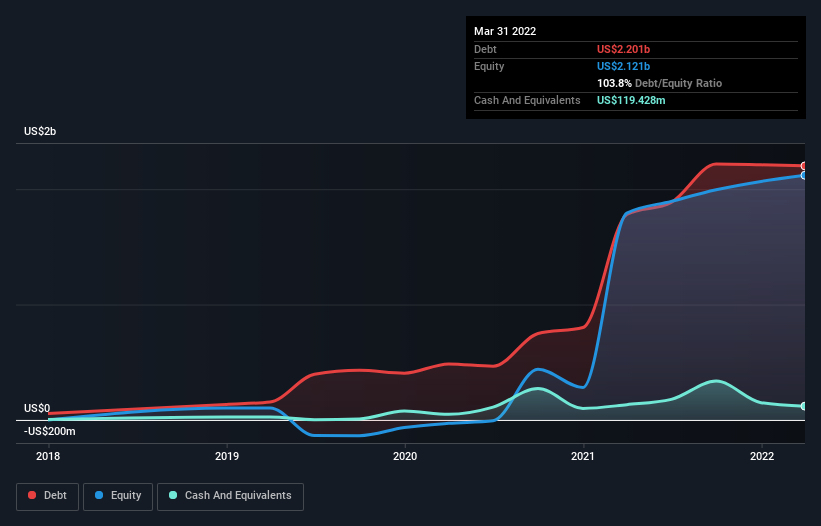

As you can see below, at the end of March 2022, AdaptHealth had US$2.20b of debt, up from US$1.78b a year ago. Click the image for more detail. On the flip side, it has US$119.4m in cash leading to net debt of about US$2.08b.

How Healthy Is AdaptHealth’s Balance Sheet?

We can see from the most recent balance sheet that AdaptHealth had liabilities of US$443.6m falling due within a year, and liabilities of US$2.64b due beyond that. On the other hand, it had cash of US$119.4m and US$369.9m worth of receivables due within a year. So its liabilities total US$2.59b more than the combination of its cash and short-term receivables.

When you consider that this deficiency exceeds the company’s US$2.54b market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

AdaptHealth’s debt is 3.6 times its EBITDA, and its EBIT cover its interest expense 2.9 times over. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. The silver lining is that AdaptHealth grew its EBIT by 105% last year, which nourishing like the idealism of youth. If that earnings trend continues it will make its debt load much more manageable in the future. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if AdaptHealth can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, AdaptHealth recorded free cash flow worth 52% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Neither AdaptHealth’s ability to cover its interest expense with its EBIT nor its level of total liabilities gave us confidence in its ability to take on more debt. But the good news is it seems to be able to grow its EBIT with ease. We should also note that Healthcare industry companies like AdaptHealth commonly do use debt without problems. We think that AdaptHealth’s debt does make it a bit risky, after considering the aforementioned data points together. That’s not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. When analysing debt levels, the balance sheet is the obvious place to start.