The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that Frontline Ltd. (NYSE:FRO) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Frontline’s Debt?

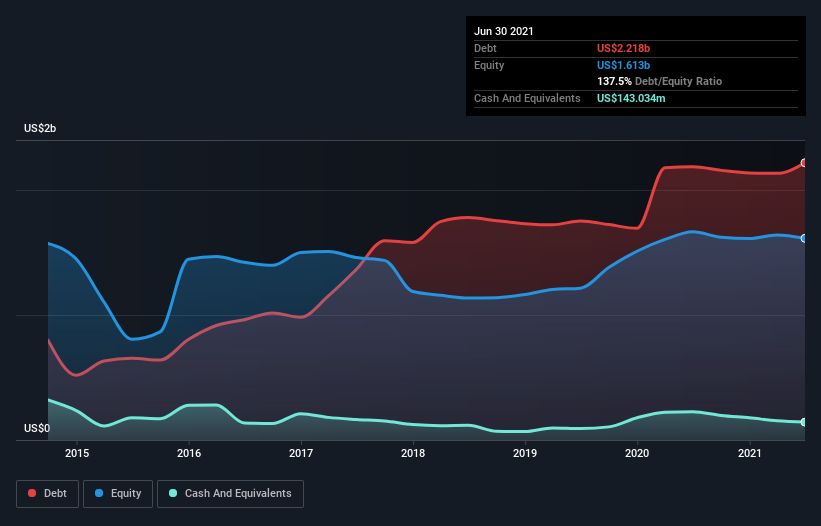

The chart below, which you can click on for greater detail, shows that Frontline had US$2.22b in debt in June 2021; about the same as the year before. However, it does have US$143.0m in cash offsetting this, leading to net debt of about US$2.07b.

How Strong Is Frontline’s Balance Sheet?

According to the last reported balance sheet, Frontline had liabilities of US$426.7m due within 12 months, and liabilities of US$1.94b due beyond 12 months. On the other hand, it had cash of US$143.0m and US$101.7m worth of receivables due within a year. So it has liabilities totalling US$2.12b more than its cash and near-term receivables, combined.

When you consider that this deficiency exceeds the company’s US$1.62b market capitalization, you might well be inclined to review the balance sheet intently. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Weak interest cover of 1.8 times and a disturbingly high net debt to EBITDA ratio of 9.3 hit our confidence in Frontline like a one-two punch to the gut. This means we’d consider it to have a heavy debt load. Even worse, Frontline saw its EBIT tank 85% over the last 12 months. If earnings keep going like that over the long term, it has a snowball’s chance in hell of paying off that debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Frontline can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we always check how much of that EBIT is translated into free cash flow. Considering the last three years, Frontline actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

On the face of it, Frontline’s net debt to EBITDA left us tentative about the stock, and its EBIT growth rate was no more enticing than the one empty restaurant on the busiest night of the year. And even its interest cover fails to inspire much confidence. Considering all the factors previously mentioned, we think that Frontline really is carrying too much debt. To our minds, that means the stock is rather high risk, and probably one to avoid; but to each their own (investing) style. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.