Cullen/Frost Bankers (CFR)

Another financial holding company, Cullen/Frost controls over $33 billion in assets. All of the company’s operations are in the state of Texas, underscoring the sheer size of the second largest state. As with most large, full-service banks, Cullen/Frost provides banking, investment, and insurance services to both business and individual clients and account holders.

CFR posted an earnings beat in its recent Q3 report, showing $1.73 EPS against the forecast of $1.69. While the 2.4% beat was welcome news, EPS was down 5 cents compared to the year-ago quarter. Quarterly revenue, at $365.8 million, was in-line with the estimates, and 3.5% higher than last year’s Q3. The stock is up 6.3% year-to-date, which makes sense considering the solid earnings.

On the negative side, CFR’s expenses were up even more steeply than the revenues. Non-interest expenses leapt up 7.8% in the last 12 months, reaching $208.9 million.

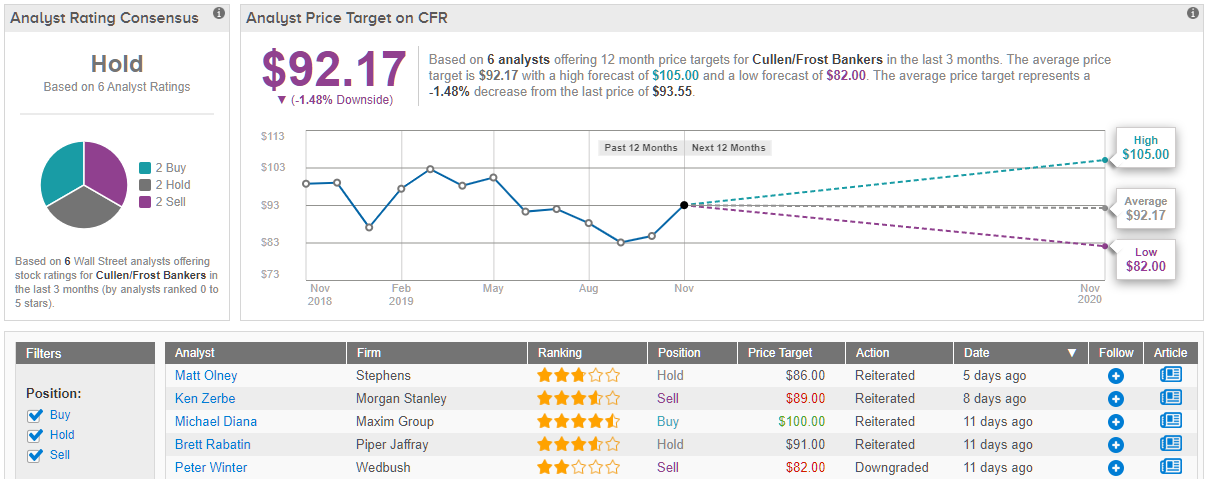

The sharp jump in expenses was on the mind of Wedbush analyst Peter Winter, when he took the step of downgrading CFR from Hold to Sell. Winter wrote, “While most banks are looking for ways to slow expense growth in a tougher revenue environment, CFR has no plans to curtail investment spending as they believe it will lead to long-term gains. As a result, they will incur some near-term pain as 2020 expense growth will increase north of 8%…” Winter expects the ‘pain’ of high expenses to continue into 2021, and to push EPS down for the next three years. In line with his bearish stance, Winter cut his price target on CFR by 6%, to $82. This implies a 12% downside.

Ultimately, the word on the Street points to a sidelined majority on CFR. In the last three months, the stock has landed 2 “buy,” 2 “hold,” and 2 “sell,” ratings. It’s clear that Wall Street is largely divided between the bulls, bears and the fence sitters when it comes to CFR’s prospects. Meanwhile, the consensus average price target points to $92.17 — a slight downside potential from Monday’s closing price.