Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, ePlus inc. (NASDAQ:PLUS) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is ePlus’s Net Debt?

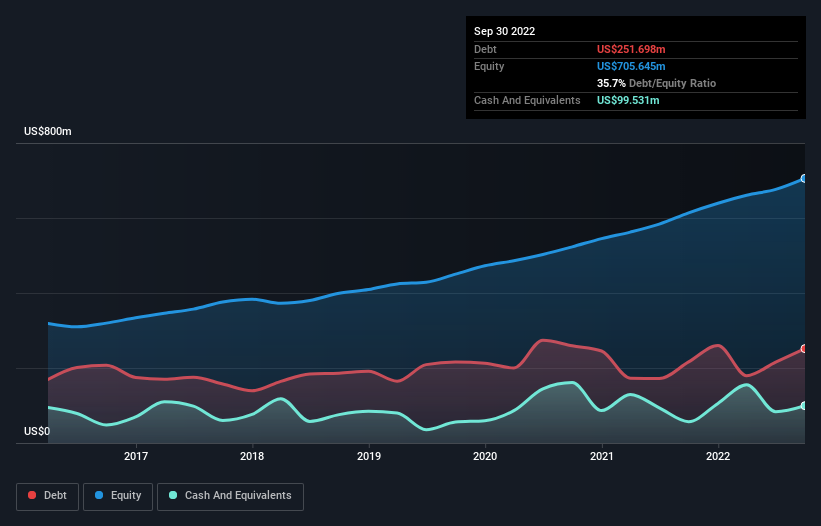

The image below, which you can click on for greater detail, shows that at September 2022 ePlus had debt of US$251.7m, up from US$216.2m in one year. However, it also had US$99.5m in cash, and so its net debt is US$152.2m.

A Look At ePlus’ Liabilities

According to the last reported balance sheet, ePlus had liabilities of US$607.3m due within 12 months, and liabilities of US$58.4m due beyond 12 months. On the other hand, it had cash of US$99.5m and US$569.5m worth of receivables due within a year. So its total liabilities are just about perfectly matched by its shorter-term, liquid assets.

Having regard to ePlus’ size, it seems that its liquid assets are well balanced with its total liabilities. So it’s very unlikely that the US$1.29b company is short on cash, but still worth keeping an eye on the balance sheet.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

ePlus has a low net debt to EBITDA ratio of only 0.89. And its EBIT covers its interest expense a whopping 108 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. And we also note warmly that ePlus grew its EBIT by 14% last year, making its debt load easier to handle. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if ePlus can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, ePlus recorded negative free cash flow, in total. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

On our analysis ePlus’s interest cover should signal that it won’t have too much trouble with its debt. However, our other observations weren’t so heartening. To be specific, it seems about as good at converting EBIT to free cash flow as wet socks are at keeping your feet warm. Considering this range of data points, we think ePlus is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it.