The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Core Laboratories N.V. (NYSE:CLB) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Core Laboratories’s Net Debt?

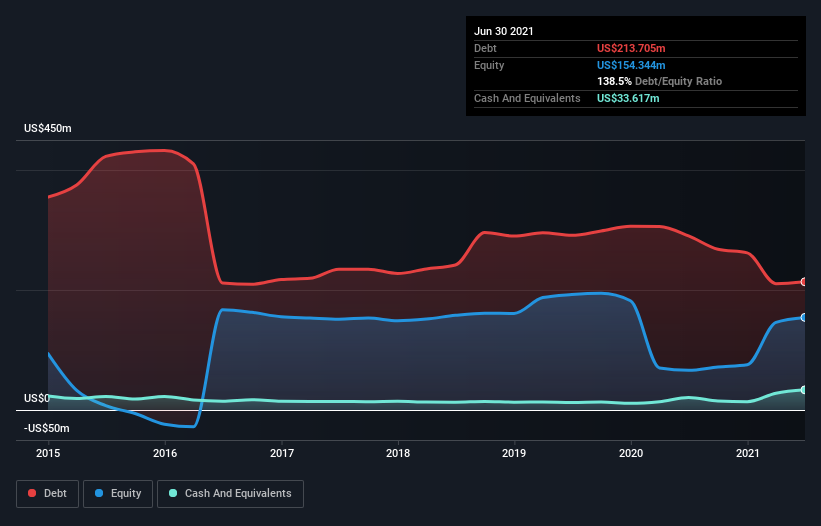

As you can see below, Core Laboratories had US$213.7m of debt at June 2021, down from US$290.2m a year prior. On the flip side, it has US$33.6m in cash leading to net debt of about US$180.1m.

How Strong Is Core Laboratories’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Core Laboratories had liabilities of US$90.9m due within 12 months and liabilities of US$353.2m due beyond that. Offsetting these obligations, it had cash of US$33.6m as well as receivables valued at US$110.2m due within 12 months. So it has liabilities totalling US$300.3m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Core Laboratories has a market capitalization of US$1.43b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Core Laboratories has a debt to EBITDA ratio of 2.7 and its EBIT covered its interest expense 4.2 times. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. Worse, Core Laboratories’s EBIT was down 40% over the last year. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Core Laboratories’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, Core Laboratories recorded free cash flow worth 77% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Core Laboratories’s EBIT growth rate was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. For example its conversion of EBIT to free cash flow was refreshing. We think that Core Laboratories’s debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. The balance sheet is clearly the area to focus on when you are analysing debt.