Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Darling Ingredients Inc. (NYSE:DAR) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Darling Ingredients’s Net Debt?

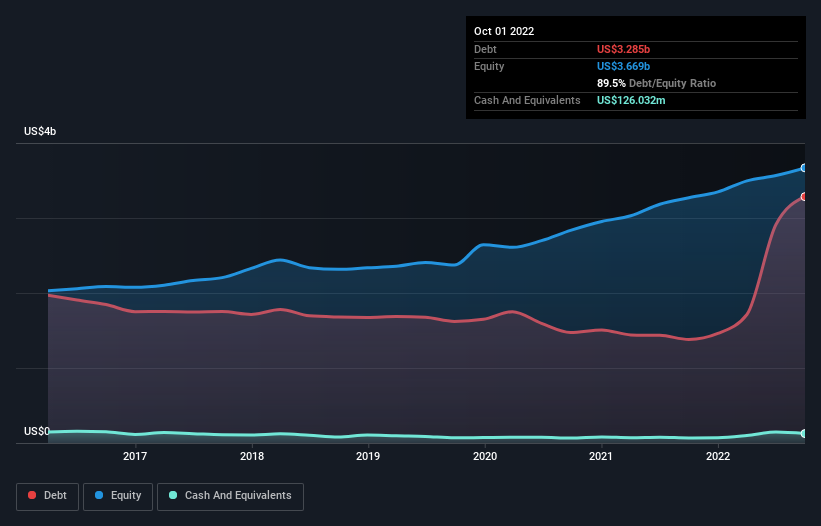

The image below, which you can click on for greater detail, shows that at October 2022 Darling Ingredients had debt of US$3.28b, up from US$1.38b in one year. On the flip side, it has US$126.0m in cash leading to net debt of about US$3.16b.

A Look At Darling Ingredients’ Liabilities

According to the last reported balance sheet, Darling Ingredients had liabilities of US$1.03b due within 12 months, and liabilities of US$4.11b due beyond 12 months. Offsetting this, it had US$126.0m in cash and US$687.3m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$4.33b.

This deficit isn’t so bad because Darling Ingredients is worth a massive US$10.7b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With net debt to EBITDA of 3.0 Darling Ingredients has a fairly noticeable amount of debt. On the plus side, its EBIT was 7.3 times its interest expense, and its net debt to EBITDA, was quite high, at 3.0. It is well worth noting that Darling Ingredients’s EBIT shot up like bamboo after rain, gaining 57% in the last twelve months. That’ll make it easier to manage its debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Darling Ingredients can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Darling Ingredients recorded free cash flow worth a fulsome 91% of its EBIT, which is stronger than we’d usually expect. That puts it in a very strong position to pay down debt.

Our View

The good news is that Darling Ingredients’s demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. But, on a more sombre note, we are a little concerned by its net debt to EBITDA. Taking all this data into account, it seems to us that Darling Ingredients takes a pretty sensible approach to debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns.