Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Corning Incorporated (NYSE:GLW) does use debt in its business. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Corning’s Net Debt?

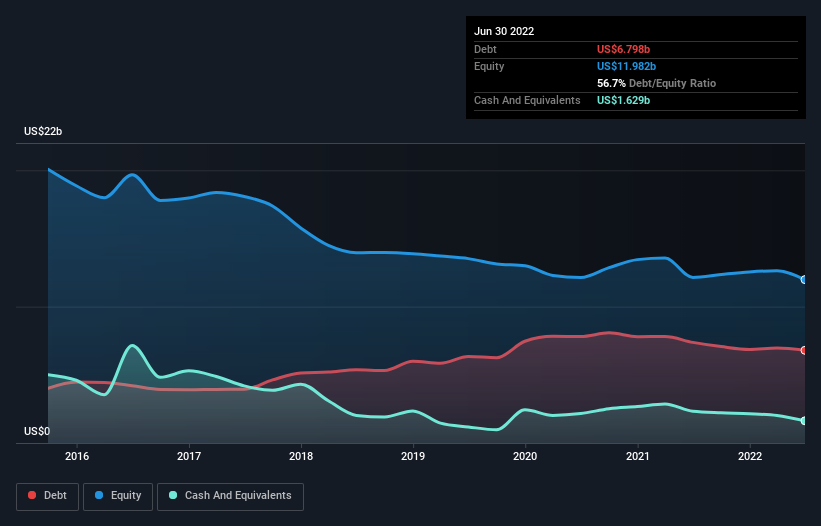

The image below, which you can click on for greater detail, shows that Corning had debt of US$6.80b at the end of June 2022, a reduction from US$7.38b over a year. On the flip side, it has US$1.63b in cash leading to net debt of about US$5.17b.

How Strong Is Corning’s Balance Sheet?

The latest balance sheet data shows that Corning had liabilities of US$5.53b due within a year, and liabilities of US$12.2b falling due after that. On the other hand, it had cash of US$1.63b and US$1.79b worth of receivables due within a year. So it has liabilities totalling US$14.3b more than its cash and near-term receivables, combined.

Corning has a very large market capitalization of US$28.4b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

With net debt sitting at just 1.4 times EBITDA, Corning is arguably pretty conservatively geared. And it boasts interest cover of 8.2 times, which is more than adequate. The good news is that Corning has increased its EBIT by 6.2% over twelve months, which should ease any concerns about debt repayment. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Corning’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Corning produced sturdy free cash flow equating to 75% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

The good news is that Corning’s demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. But truth be told we feel its level of total liabilities does undermine this impression a bit. All these things considered, it appears that Corning can comfortably handle its current debt levels. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it’s worth monitoring the balance sheet. The balance sheet is clearly the area to focus on when you are analysing debt.