The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Ciena Corporation (NYSE:CIEN) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Ciena’s Net Debt?

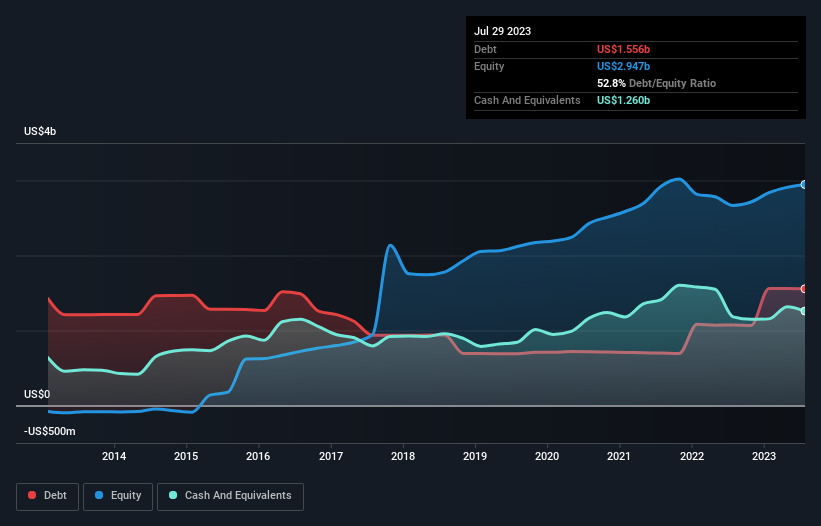

The image below, which you can click on for greater detail, shows that at July 2023 Ciena had debt of US$1.56b, up from US$1.07b in one year. However, it also had US$1.26b in cash, and so its net debt is US$296.1m.

A Look At Ciena’s Liabilities

The latest balance sheet data shows that Ciena had liabilities of US$965.7m due within a year, and liabilities of US$1.81b falling due after that. Offsetting this, it had US$1.26b in cash and US$1.16b in receivables that were due within 12 months. So its liabilities total US$359.0m more than the combination of its cash and short-term receivables.

Since publicly traded Ciena shares are worth a total of US$6.68b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

With net debt sitting at just 0.57 times EBITDA, Ciena is arguably pretty conservatively geared. And it boasts interest cover of 9.0 times, which is more than adequate. Another good sign is that Ciena has been able to increase its EBIT by 21% in twelve months, making it easier to pay down debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Ciena can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Looking at the most recent three years, Ciena recorded free cash flow of 23% of its EBIT, which is weaker than we’d expect. That’s not great, when it comes to paying down debt.

Our View

The good news is that Ciena’s demonstrated ability handle its debt, based on its EBITDA, delights us like a fluffy puppy does a toddler. But truth be told we feel its conversion of EBIT to free cash flow does undermine this impression a bit. Taking all this data into account, it seems to us that Ciena takes a pretty sensible approach to debt. While that brings some risk, it can also enhance returns for shareholders.