With the agreement to sell its stake in the Airbus A220 program, Bombardier (OTCQX:BDRAF) has formalized its departure from the commercial aerospace industry. In this report, we have a closer look at the sum that Bombardier received for its stake in the Airbus A220 program and explain why this is an incredibly disappointing outcome for Bombardier.

Exiting commercial aviation

As we know now, Bombardier will be exiting the commercial aviation industry and that hardly should come as a surprise given that the C Series program stalled further investments in Bombardier’s other commercial aircraft, the CRJ (regional jet) and Q400 (turboprop). Bombardier did come up with an iteration of the CRJ in 2007, but other than it was meeting the limits of its programs with costly new developments being required to become more competitive. Bombardier simply did not have that money as it tied its success of its commercial aviation business to the C Series.

In a note to investors in 2017, we already pointed out that Bombardier would likely cease its commercial aviation arm with the C Series being majority owned by Airbus:

Bombardier will likely completely remove itself from Commercial Airplanes business, keeping the duopoly alive.

That removal from the commercial aviation business started in November 2018 as Bombardier sold its Q400 program to De Havilland Aircraft of Canada with gross proceeds of $298 million. In June 2019, the sale of CRJ program including the maintenance, support, refurbishment, marketing, and sales activities to Mitsubishi Heavy Industries (OTCPK:MHVYF) followed for $550 million in cash and $200 million in liabilities to be assumed. The transaction is expected to close in the second half of 2020.

With the Airbus A220 stake in the joint venture being sold, the divestiture from the commercial aviation business is complete.

Aerostructures exit is a painful one

We’ve been looking at Bombardier’s commercial aviation business for years and we can only conclude that divesting made sense. Losing the C Series is of course painful, but with negotiated agreement, it was rather clear that Bombardier couldn’t come out of it as a winner. What’s a bit more painful is the aerostructures sale. If Bombardier were to exit commercial aviation, selling the Aerostructures business as well would make sense.

However, by doing so the company lost its operations in Belfast which produces the Airbus A220 wings. So, divesting from Aerostructures means that Bombardier could benefit even less from the Airbus A220 success. In fact, by divesting the operations in Belfast, Casablanca, Querétaro and Dallas, Bombardier is benefiting even less from the growing commercial aviation industry in which it could have played a role given that Bombardier Aerostructures also produces parts for the Airbus A320neo and the Q400. The big scale down of the aerostructures business means that even as a supplier and after-market services provider, Bombardier lost its momentum. The sale of the Aerostructures business wasn’t an odd one, but I believe it certainly wasn’t a preferred one.

Airbus A220 Ends Bombardier’s aspirations in Commercial Aviation

While the Aerostructures exit already was painful, the Airbus A220 exit is devastating. It would be delusional to say that Bombardier would have made the Airbus A220 a success all by itself, because they really wouldn’t. They have been looking for partners to cover production costs since 2015 and they have been able to count on the Québec government to keep the company afloat. What still holds is that Bombardier got an extremely small amount of money for its share in the Airbus A220 program

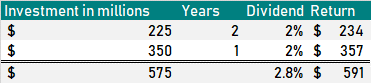

The agreement between Airbus and Bombardier called for Bombardier to cover production losses of $225 million in 2018, $350 million in 2019 and $350 million in 2020-2021 before additional production losses would be carried by Class A shareholders of Airbus Canada Limited Partnership. The agreement also laid out that Bombardier could ask Airbus to acquire its stake prior to the 7.5-year window after which the call and put right both manufacturers have would be exercisable. Bombardier used that option and what they received for that is a tiny fee of 2% annual dividends on their investment.

The calculation valuing Bombardier’s share is very easy:

In Q3, Bombardier’s share in the program was still valued at $1.88B. Back then Bombardier already had hinted on a write down on the program. Given the slower than anticipated progress and Bombardier removing itself from the program, I expected the program to see a $554 million write down and expected that Bombardier’s share in future capital contributions would be used to value the Airbus A220 as a product. This would put the value on $1.325B, which is the value I shared in a previous report.

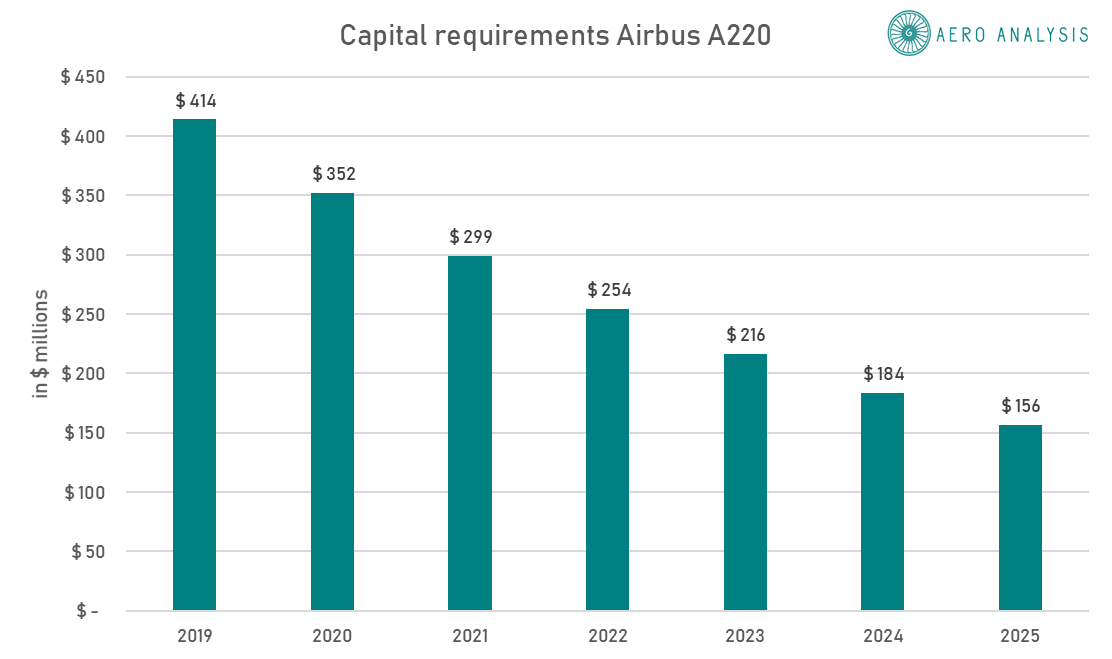

Figure 1: Estimated capital requirements Airbus A220

Figure 1 shows our estimate on the capital requirements for the Airbus A220 program through 2025. From 2021-2025, I expected that some $1.1B would be required from all Class A shareholders of the Airbus Canada Limited Partnership. For Bombardier that would boil down to $377 million plus the $350 million that it would still be obliged to contribute in 2020. If we correct the partnership value for the expected future capital contributions from Bombardier that would bring the partnership value to $1.15B. That’s a sum Bombardier didn’t receive. Even if we consider the time value of the money, we would still get to $1.03B, which is 75% higher than what Bombardier got for its stake.

To me it seems that while Bombardier received a fee on its investment, the actual share in the program was worth far more. There’s one way in which the investment value aligns with the program value and that’s if we reduce the $1.88B by future capital contributions that Bombardier was expected to make amounting to $727 million and reduce it with $554 million contributions that we expected Airbus to make. That would bring the value to $599 million, which is 8 million higher than what Bombardier will be receiving now.

We also checked whether our estimate on future capital contributions for Bombardier was accurate and from Bombardier’s annual report we found that our estimate differed by just $27 million:

On February 12, 2020, Bombardier entered into an agreement with Airbus SE and the Government of Quebec, under which Bombardier transferred its shares in the Airbus Canada Limited Partnership (OTC:ACLP) to Airbus and the Government of Quebec, improving Bombardier’s cash position. This includes cash proceeds of approximately $600 million from Airbus, of which $531 million was paid upon closing with the balance to be paid over 2020-21, and the elimination of all future capital requirements for the A220 program, estimated at approximately $700 million.

Conclusion

For Bombardier the Airbus A220 ends with a headache. The company accumulated debt to penetrate the highly profitable single aisle market, but it simply didn’t have enough funds to carry itself to the stage were production would become profitable. In the process, it had to scrap investments in other programs which weakened its position on the commercial aviation market and the agreement with Airbus wasn’t necessarily beneficial for Bombardier’s prospects, but was beneficial for the Airbus A220.

Bombardier has disposed its stake in the Airbus A220 program for just $591 million, merely valuing the investment it made on production losses, while the company spent around $7.4B developing the Bombardier C Series and damaged its remaining commercial aviation business to the extent that it wasn’t worth much more than a $1 billion. The CRJ and Q400 programs were worth around $1B, which I think also was the value of the Airbus A220 program. Yet this advanced program was valued at just $591 million. The way the agreement with Airbus was structured, Bombardier’s financial position and Airbus’ extensive network and investments in an additional production line didn’t give Bombardier much leverage to negotiate a better deal. The agreement was specifically structured as such. Airbus didn’t even need to heavily discount Bombardier’s share in case it would withdraw from the joint venture. To me it still seems that Airbus is underpaying Bombardier by roughly $560 million reducing the cash consideration by what Airbus would spend in the coming years on the program, but Bombardier knew what it signed for so, in 2017, with the ink still drying they could have known they wouldn’t get much for the Airbus A220. Bombardier made a brave step, but they found out the hard way that bigger is not always better and that it takes more than good product to enter the highly profitable single aisle market.

In my first piece on Bombardier in 2020, I pointed out that more value could be generated by spinning off the businesses instead of keeping them under the Bombardier umbrella. Prior to announcing the sale of the Transportation business, Bombardier shares gained 12%. With the news of Bombardier selling its train division out, shares have lost 9% of their value and our now up only modestly compared to the price point at the time of writing my initial piece. So, it seems to be a case of “buy the rumor, sell the fact,” possibly in combination with some valid concerns on the business jet business. What holds is that Bombardier is now in a much better liquidity position to pay off its debt, but it might no longer be the kind of company that gets a lot of interest from investors.