Bombardier (OTCQX:BDRAF) is currently in a difficult spot. In 2019, its five-year turnaround plan setting objectives went bust while debt will start maturing starting 2021. In this report, we have a quick look at how Bombardier got in this situation and what its options are.

Bombardier carries debt load without benefits

We could do an entire analysis on where it went wrong with Bombardier, possibly that’s something we will do in the future, but, for now, we can point at two things that really complicated Bombardier’s path. Years ago, Bombardier decided to enter the highly profitable single aisle market with a 100-140 seat aircraft that would directly challenge the core business of Airbus (OTCPK:EADSF) and Boeing (BA) at the lower side of the seating range. Aircraft developments are costly, and for Bombardier developing the C Series was no exception if you add delays to that the costs rose north of $6B.

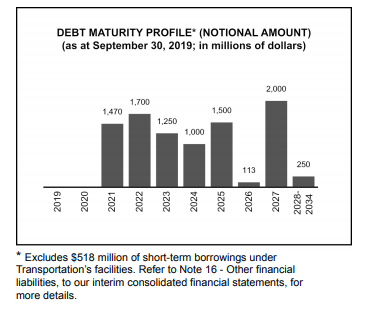

As Bombardier’s debt maturity profile shows, the company has slightly over $9B in debt maturing up to and including 2027 and $250 million in the 2028-2034 frame and $518 million of short-term borrowings. So, the total is nearly $9.8B, of which $9.55B will mature until 2027. The development costs for the C Series play a role in that. With development costs north of $6B it accounts for more than 60% of Bombardier’s debt load. Bombardier took on that debt assuming it would one day rake in the full profits. However, driven by schedule delays and associated costs and a feud with Boeing (which it won), the program was driven in the hands of Airbus which acquired a 50.01% stake, leaving Bombardier with a 34% share in the program while Bombardier’s cash pile declined from $3.4B a couple of years ago to little over $2.25B in Q3 2019.

While the maturity profile is closing in on the company, the cash pile is declining, driven by a delay in production cost improvements on the Airbus A220 program and additional investments required to keep train projects on schedule. For 2019, Bombardier has preliminarily guided for a negative $1.2B free cash flow, which could mean that the cash pile remains even for the year in the best-case scenario. With the cash at hand, Bombardier can easily pay off debt of $1.5B maturing in 2021, but it will bring the company low on cash, meaning that the company doesn’t have a lot of flesh on the bones to cope with additional cost growth. So, instead, the company has been looking to sell parts of its business.

Bringing the company to the chopping block

With the cash pile declining, Bombardier has started to sell parts of its business to raise cash. That’s nothing new. In 2015, Bombardier sold its military aviation training activities to CAE following by a $645 million sale of the business jet training activities in 2018. The net proceeds received were $532 million.

In November 2018, Bombardier sold its Q400 program to De Havilland Aircraft of Canada with gross proceeds of $298 million.

In June 2019, Bombardier announced it sold the CRJ program including the maintenance, support, refurbishment, marketing, and sales activities to Mitsubishi Heavy Industries (OTCPK:MHVYF) for $550 million in cash and $200 million in liabilities to be assumed. The transaction is expected to close in the second half of 2020.

In October 2019, Bombardier announced it would be selling its Aerostructures business to Spirit AeroSystems (SPR) for $500 million in cash and $700 million in liabilities to be assumed by Spirit AeroSystems, valuing the business at 10 times earnings. The transaction is expected to close in the first half of 2020.

If we look at sales that should be concluded this year, then Bombardier should be getting $1.05B in cash and $0.7B in liabilities to be assumed by other parties. Assuming all these liabilities are debts (which is not necessarily true) and all cash will be used to reduce the debt load, then Bombardier will be able to reduce its debt load by $1.75B or 20% of its debt that’s set to mature by 2027. Basically, Bombardier is selling parts of its business to raise cash and reduce liabilities.

In the turnaround plan, Bombardier set a >$10B revenue target and >9% EBIT margin for Transportation and >$8.5B in revenues and 8-10% EBIT margin for its business jet segment. Combined that would lead to $1.78B in EBIT while the company targeted $750 million to $1B for all of its core businesses. With Bombardier selling part of its businesses (all of which should have contributed to free cash flow by 2020) and the turnaround plan going bust, the $1B free cash flow objective seems to be out of reach, meaning that with the existing business segments Bombardier would rely on its cash pile and additional borrowings to make its debt repayments. Having to borrow cash to make debt repayments is something we see happening with Boeing today as well.

Which part to sell?

Bombardier has $2.6B in cash and $1.1B in cash due for 2020. So, on the condition that the company generates positive free cash flow in 2020 and onward, it can pay off its debt set to mature by 2022. The big question is how to proceed from there as the cash flow profile might not be sufficient to cover debt repayment in future years. It could, of course, look to borrow more, but one can question how prudent that would be for a company that struggles to generate a $1B free cash flow for years now. The other option is divesting.

Divestiture of train business

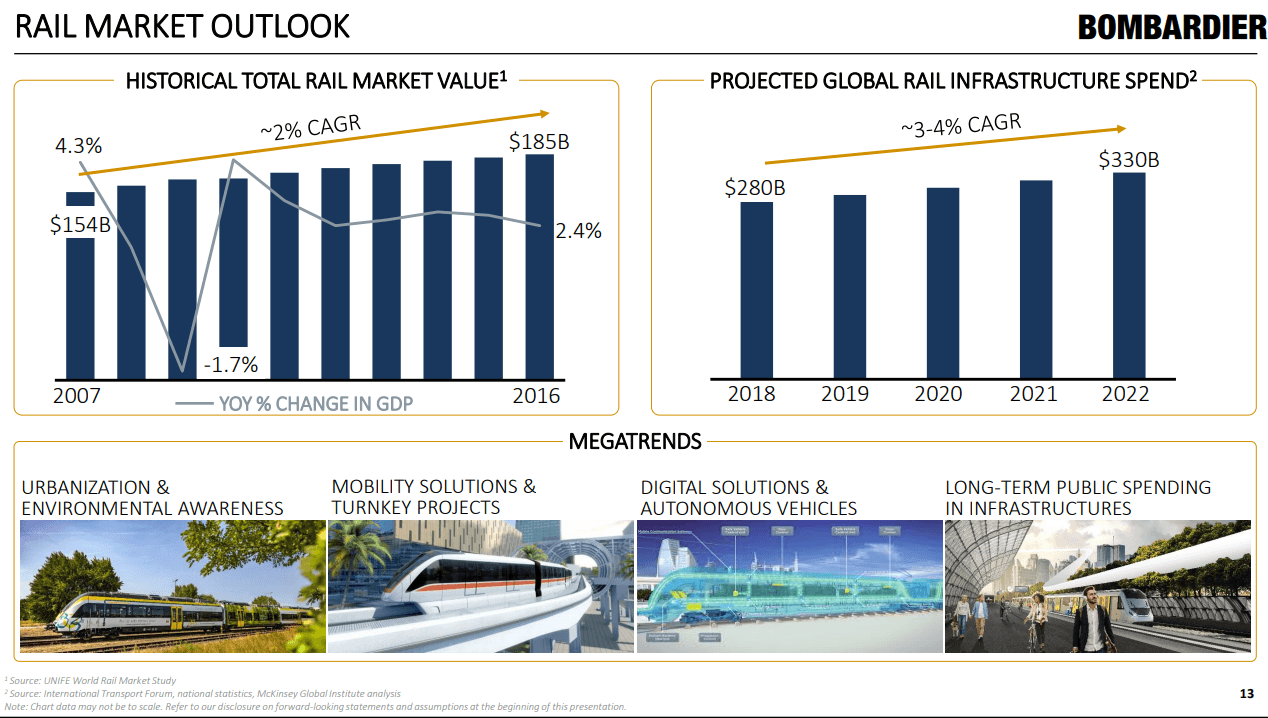

Bombardier’s Transportation business has been a drag on the company’s results in 2019. Getting rid of it does seem plausible with that in mind. The rail infrastructure has a CAGR of 3% to 4% vs. 2% for the total rail market value with Bombardier being positioned with a ~$36B backlog. If Bombardier gets it right, this is a segment that should bolster the company’s earnings and cash. However, we also have read about multiple instances in which Bombardier trains were refused due to lacking quality. One such example is from Deutsche Bahn refusing to take delivery of 25 trains.

Bombardier had previously targeted a 10% EBIT margin and $10B in revenues. Valuing the company at 10 times EBITDA, with an EBITDA margin of 9.5% (as achieved in 2018) and $7.5B in revenues as Bombardier expects for the full year. The Transportation business would be valued $7.125 billion, though that value could be lower. Bombardier’s stake of 70% would be worth roughly $5B.

Together with the $1.1B coming from divestitures to be completed in 2020, $700 million in liabilities to be transferred (all assumed to be debt) that would cover 70% of Bombardier’s maturing debt profile. The company has cash on hand to cover all the way up to 96%. So, divesting the train business seems like a big deal for Bombardier to be able to repay debt. The positive would be that the company no longer would be plagued from cost growth on train projects and competition from China, while the negative would be that this segment seems to provide better scalability than the business jet segment.

Divestiture of business jet segment

The other option for Bombardier would be to divest the business jet segment. It would be another example of Bombardier losing a product it attributed many resources to, so for that reason it wouldn’t be preferable. One reason that makes divesting the business jet preferable is that the business jet segment focuses on the super rich. It’s a market that doesn’t scale well and expected deliveries per annum have been around 600-700 deliveries for years now. Bombardier is positioned well on that market, I believe, but it’s also a competitive one with many players hunting for the same buck so a round of consolidation wouldn’t be completely unexpected. Textron (TXT) has been interested in Bombardier’s business. I believe Bombardier’s business jet unit would be a complementary fit to Textron’s business line up. The big question again is what the unit is worth. At 2020 targeted revenues of >$8.5B and an 8% to 10% EBIT margin, the annual earnings would be $680-850 million. At 10 times earnings that would boil down to $6.8B-8.5B, and I would expect the business to be valued closer to the lower end of the range. Divestiture of the business jet unit would cover 70% of Bombardier’s debt to mature until 2027 and almost 90% including liabilities relief and cash considerations for 2020. Including Bombardier’s cash on hands, the debt would be fully covered.

Divestiture of Airbus A220 joint venture

The last divestiture possible would be a withdrawal from the Airbus A220 program, which I think makes sense given that Bombardier has to make significant investments in the program, while the program possibly won’t be profitable until 2022, years before Airbus likely will buy Bombardier’s share. Given that cash infusions will be required in 2020-2021, it’s unlikely that Bombardier will benefit from the investments it’s required to make now and selling the share in the joint venture to Airbus now wouldn’t be a bad idea.

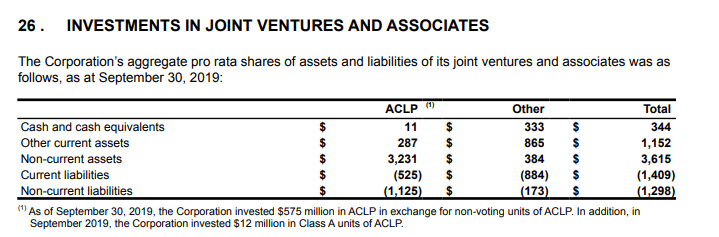

If we look at how Bombardier has valued the ACLP joint venture, I’d say that things don’t look quite rosy. The assets total $3.5B, which is a nice sum to get for the Bombardier share in the joint venture. However, there also is $1.65B in liabilities. That would value Bombardier’s share of the joint venture at $1.88B and the company is expected to write off on the value in its Q4 and full-year earnings report. An alternative way to value the business, per the agreement, would be to compensate Bombardier for its investment in the program since the joint venture was established and apply a 2% interest rate, which would bring the proceeds to $591 million if Airbus were to buy Bombardier’s stake now.

Note: While this report was in the queue for publishing, Bombardier announced that it had divested from the Airbus A220 joint venture.

Conclusion

Bombardier is in a difficult spot with >$9B in debt maturing in the coming years. Two divestitures that will be completed this year should allow Bombardier to make debt repayments for 2021. I do believe that for further debt repayments the company will have to look to either sell its business jet division or its rail business as a divestiture of the A220 joint venture isn’t enough. Bombardier will have to choose whether it wants to focus on the rail business where it has recently experienced significant headwinds or whether it wants to focus on business jets, where it recently launched a new product but with the drawback of the market being a crowded one with limited possibilities to grow as business jet deliveries have been stagnant for years. Divesting the business jet unit would be a disappointment as it would be yet another good product that Bombardier developed falling into the hands of another company, which is what will happen to the C Series that already carries Airbus’ name. Either way, what we see is that Bombardier choked on the development of the C Series aircraft, which still is a phenomenal aircraft, and with a turnaround around plan going bust the company is now taking parts of its business and selling them in an effort to survive.