Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies AtriCure, Inc. (NASDAQ:ATRC) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

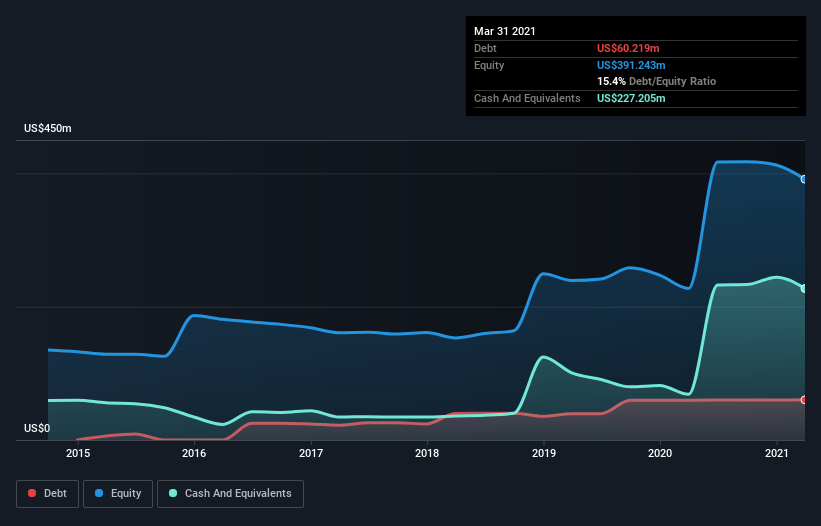

What Is AtriCure’s Net Debt?

As you can see below, AtriCure had US$60.2m of debt, at March 2021, which is about the same as the year before. You can click the chart for greater detail. But on the other hand it also has US$227.2m in cash, leading to a US$167.0m net cash position.

A Look At AtriCure’s Liabilities

We can see from the most recent balance sheet that AtriCure had liabilities of US$58.5m falling due within a year, and liabilities of US$250.2m due beyond that. On the other hand, it had cash of US$227.2m and US$29.7m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$51.7m.

This state of affairs indicates that AtriCure’s balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it’s very unlikely that the US$3.66b company is short on cash, but still worth keeping an eye on the balance sheet. While it does have liabilities worth noting, AtriCure also has more cash than debt, so we’re pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if AtriCure can strengthen its balance sheet over time.

In the last year AtriCure had a loss before interest and tax, and actually shrunk its revenue by 7.6%, to US$213m. We would much prefer see growth.

So How Risky Is AtriCure?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that AtriCure had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$18m and booked a US$49m accounting loss. But at least it has US$167.0m on the balance sheet to spend on growth, near-term. Summing up, we’re a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. When analysing debt levels, the balance sheet is the obvious place to start.