Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that American Eagle Outfitters, Inc. (NYSE:AEO) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does American Eagle Outfitters Carry?

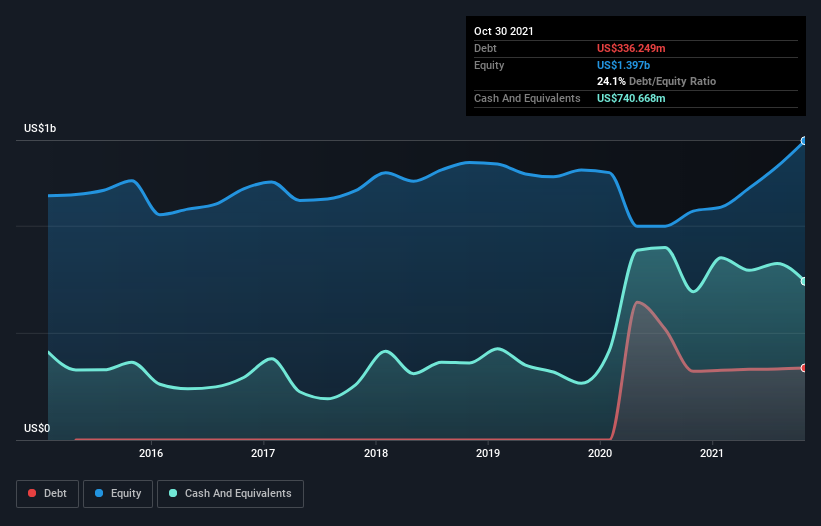

You can click the graphic below for the historical numbers, but it shows that as of October 2021 American Eagle Outfitters had US$336.2m of debt, an increase on US$321.1m, over one year. However, it does have US$740.7m in cash offsetting this, leading to net cash of US$404.4m.

How Healthy Is American Eagle Outfitters’ Balance Sheet?

We can see from the most recent balance sheet that American Eagle Outfitters had liabilities of US$869.6m falling due within a year, and liabilities of US$1.48b due beyond that. Offsetting these obligations, it had cash of US$740.7m as well as receivables valued at US$228.5m due within 12 months. So it has liabilities totalling US$1.38b more than its cash and near-term receivables, combined.

American Eagle Outfitters has a market capitalization of US$4.06b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. Despite its noteworthy liabilities, American Eagle Outfitters boasts net cash, so it’s fair to say it does not have a heavy debt load!

Although American Eagle Outfitters made a loss at the EBIT level, last year, it was also good to see that it generated US$620m in EBIT over the last twelve months. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if American Eagle Outfitters can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. While American Eagle Outfitters has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last year, American Eagle Outfitters’s free cash flow amounted to 27% of its EBIT, less than we’d expect. That’s not great, when it comes to paying down debt.

Summing up

Although American Eagle Outfitters’s balance sheet isn’t particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$404.4m. So we don’t have any problem with American Eagle Outfitters’s use of debt. When analysing debt levels, the balance sheet is the obvious place to start.