Summary

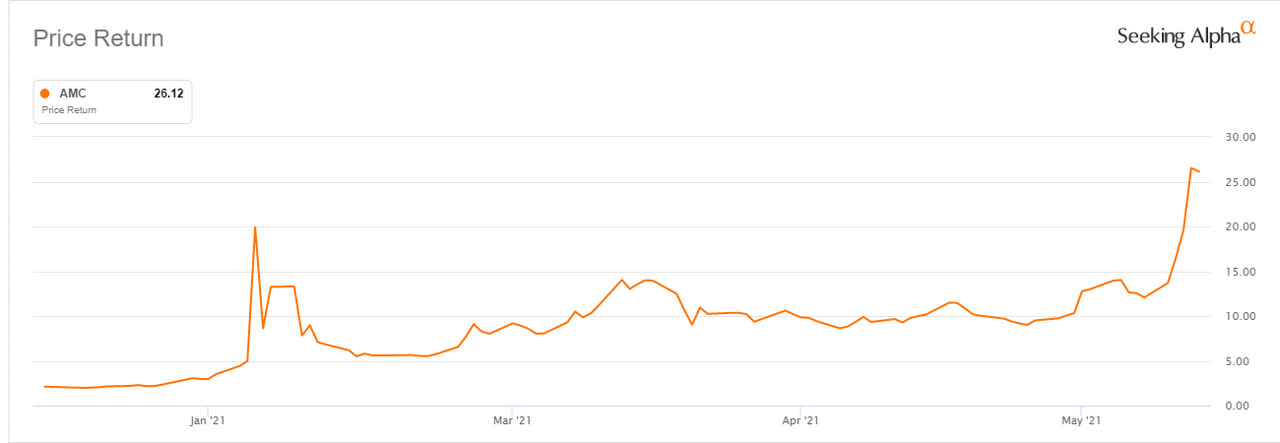

- Thanks to the help of Reddit’s Wall Street Bets community, AMC shares once again reached new record highs.

- However, the mounting interest expenses along with the high cost of servicing its debt will make it hard for the current momentum to last long.

- We believe that the current premium at which AMC trades is not justified and we might once again open a short position in the company in the upcoming days.

- Looking for a helping hand in the market? Members of Best Short Ideas get exclusive ideas and guidance to navigate any climate.

AMC Entertainment (AMC) stock has been gaining momentum in recent weeks, as traders from Reddit’s Wall Street Bets community once again decided to purchase the company’s shares in large quantities which drove stock prices higher, as they did so in late January. While these share purchases moved the stock, which now trades at record levels, there’s every reason to believe that most of the gains will evaporate in the upcoming weeks, as fundamentally AMC is a weak company in a declining industry that constantly raises money via debt and share offerings in order to sustain its losses. While this helped AMC to survive the pandemic, the mounting interest expenses along with the high cost of servicing its debt will make it hard for the business to recover anytime soon. Therefore, we believe that the current momentum in AMC’s stock is not going to last long and we might once again open a short position in the company in the upcoming days.

Lots of Risks Ahead

AMC’s stock has once again appreciated on heavy volume in recent days, as public investors, who now own the majority of the company, managed to execute another squeeze that pushed shares to record highs. However, as the company’s stock trades significantly above its pre-COVID-19 levels even though its share count increased by over 300% while the business continues to struggle, there’s a risk that such a squeeze is not sustainable in the long run. Considering that AMC’s revenues in Q1 declined by 84.2% Y/Y to $148.3 million, while at the same time the company had a net loss of $557 million during the period, we believe that the current premium at which AMC trades is not justified and there’s every reason to believe that the current momentum is not going to last long.

The good thing about AMC is that it managed to raise enough liquidity in order to not to worry about any insolvency issues in the short term. While at the end of Q1 the company had $813.1 million in cash reserves, in late April it executed another at-the-market offering and sold 43 million additional shares at $9.94 per share under the previous authorization program, which helped it to increase its liquidity to around $1.2 billion.

However, the high debt burden along with high-interest expenses will make it extremely hard for the business to create any value at all in the upcoming quarters. At the end of Q1, AMC still had $5.44 billion in long-term debt and its interest expense at the end of the quarter stood at $153 million. While the proceeds from the latest share offering will be spent on covering its high-interest debt first, the company is still likely going to spend around $600 million in interest expenses this year. Considering that before the pandemic in 2019 AMC generated only $579 million in cash from operations, it will be extremely hard for the company to last long without raising additional liquidity, especially in the current depressed business environment where it’s unlikely that any FCF will be generated at all anytime soon. Therefore, it’s safe to assume that an overleveraged balance sheet is here to stay.

The reality is that AMC is very likely going to raise even more liquidity in the long run only to sustain its current losses, as it’s unlikely that the business will recover from the pandemic anytime soon. Therefore, even if the company manages to cover its most expensive debt, it’ll still have a significant debt burden, which will prevent the business from growing and will make it nearly impossible for AMC to service the rest of its debt without raising additional liquidity. In our latest article on AMC, we’ve said that the company believes that in order to not run out of cash in the next few quarters, it needs to operate at a capacity of ~90% pre-pandemic levels, and we don’t see that happening anytime soon.

If AMC fails to raise additional debt, then another secondary offering will be its only solution, which in the end will dilute its shareholders even more. While the company initially planned to ask its shareholders to authorize the option to offer additional 500 million shares and even pledged not to issue them this year, it later decided to withdraw that request. However, AMC has also postponed its annual investors meeting from May to late July, so there’s still a possibility that it will ask for some sort of authorization to issue additional shares in the foreseeable future, but the number of that shares might be lower than initially requested. The company clearly stated in one of its recent earnings filings that if it won’t be able to find additional liquidity in case of poor recovery of the business, then it’ll be looking at options to restructure its liabilities. Therefore, we believe that the company will have no other choice but to ask for some sort of authorization from shareholders later on in order to improve its liquidity profile.

The other problem is that even if AMC dumps 500 million additional shares onto the market, which will more than double its current share count, and covers a large portion of its debt, the growth will still be limited due to the fact that the movie industry is changing and streaming services are becoming more popular every day. On top of that, the latest data suggests that there’s no pent-up demand for movies, as the attendance in a large number of AMC’s theaters across the country is still below the permitted capacity levels. While at the end of Q1 AMC had 585 domestic theaters opened at a limited capacity from 15% to 60%, its revenues from admissions were still down 88% during the quarter to $69 million from $568 million a year ago.

The truth is that AMC is not a turnaround story. The company has extremely diluted its shareholders in recent months in order to sustain its losses, but there’s still a risk that it won’t be able to financially recover due to the weak state of the industry in which it competes. Considering this, we believe that it will be hard for the company to repair its balance sheet in the current environment and there’s every reason to believe that it will continue to burn cash just to stay alive. While currently, AMC has the momentum going for it, we believe that it’s not going to last long due to the reasons stated above, and we might once again open a short position in the company in the upcoming days.