Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies Alcoa Corporation (NYSE:AA) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Alcoa’s Debt?

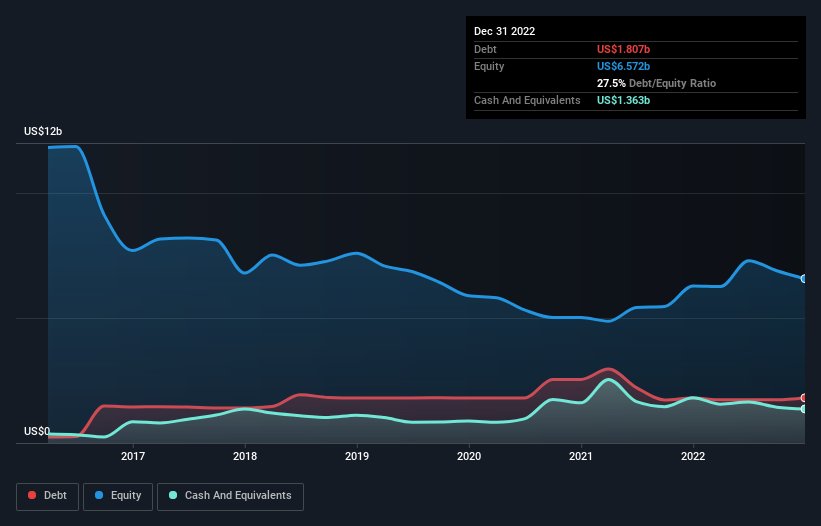

As you can see below, Alcoa had US$1.81b of debt, at December 2022, which is about the same as the year before. You can click the chart for greater detail. On the flip side, it has US$1.36b in cash leading to net debt of about US$444.0m.

How Strong Is Alcoa’s Balance Sheet?

The latest balance sheet data shows that Alcoa had liabilities of US$3.00b due within a year, and liabilities of US$5.21b falling due after that. Offsetting these obligations, it had cash of US$1.36b as well as receivables valued at US$909.0m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$5.94b.

This is a mountain of leverage relative to its market capitalization of US$8.30b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Alcoa’s net debt is only 0.22 times its EBITDA. And its EBIT covers its interest expense a whopping 13.1 times over. So we’re pretty relaxed about its super-conservative use of debt. It is just as well that Alcoa’s load is not too heavy, because its EBIT was down 33% over the last year. Falling earnings (if the trend continues) could eventually make even modest debt quite risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Alcoa can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. In the last three years, Alcoa’s free cash flow amounted to 24% of its EBIT, less than we’d expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

We’d go so far as to say Alcoa’s EBIT growth rate was disappointing. But on the bright side, its interest cover is a good sign, and makes us more optimistic. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Alcoa stock a bit risky. That’s not necessarily a bad thing, but we’d generally feel more comfortable with less leverage. There’s no doubt that we learn most about debt from the balance sheet.