Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Alaska Air Group, Inc. (NYSE:ALK) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Alaska Air Group’s Net Debt?

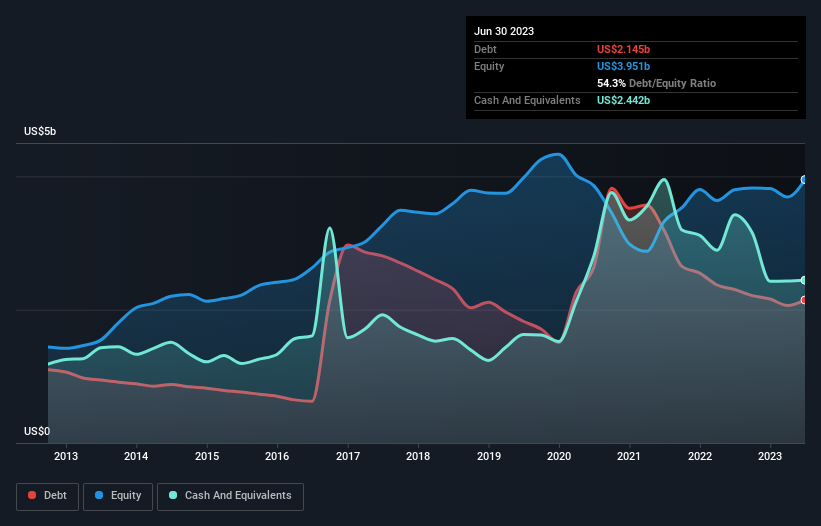

As you can see below, Alaska Air Group had US$2.15b of debt at June 2023, down from US$2.30b a year prior. But it also has US$2.44b in cash to offset that, meaning it has US$297.0m net cash.

A Look At Alaska Air Group’s Liabilities

We can see from the most recent balance sheet that Alaska Air Group had liabilities of US$5.18b falling due within a year, and liabilities of US$5.70b due beyond that. Offsetting these obligations, it had cash of US$2.44b as well as receivables valued at US$351.0m due within 12 months. So its liabilities total US$8.09b more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the US$5.32b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we’d watch its balance sheet closely, without a doubt. At the end of the day, Alaska Air Group would probably need a major re-capitalization if its creditors were to demand repayment. Given that Alaska Air Group has more cash than debt, we’re pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total.

In fact Alaska Air Group’s saving grace is its low debt levels, because its EBIT has tanked 32% in the last twelve months. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Alaska Air Group can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Alaska Air Group has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last two years, Alaska Air Group burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Summing Up

While Alaska Air Group does have more liabilities than liquid assets, it also has net cash of US$297.0m. Unfortunately, though, both its struggle EBIT growth rate and its conversion of EBIT to free cash flow leave us concerned about Alaska Air Group So even though it has net cash, we do think the business has some risks worth watching. There’s no doubt that we learn most about debt from the balance sheet.