The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Resideo Technologies, Inc. (NYSE:REZI) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

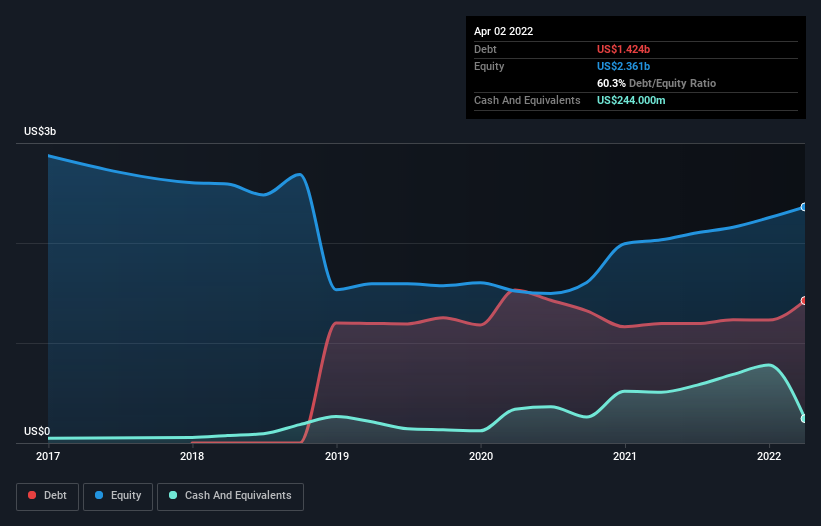

What Is Resideo Technologies’s Net Debt?

The image below, which you can click on for greater detail, shows that at April 2022 Resideo Technologies had debt of US$1.42b, up from US$1.20b in one year. However, because it has a cash reserve of US$244.0m, its net debt is less, at about US$1.18b.

A Look At Resideo Technologies’ Liabilities

The latest balance sheet data shows that Resideo Technologies had liabilities of US$1.55b due within a year, and liabilities of US$2.34b falling due after that. Offsetting this, it had US$244.0m in cash and US$1.01b in receivables that were due within 12 months. So its liabilities total US$2.63b more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of US$3.56b, so it does suggest shareholders should keep an eye on Resideo Technologies’ use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

We’d say that Resideo Technologies’s moderate net debt to EBITDA ratio ( being 1.7), indicates prudence when it comes to debt. And its strong interest cover of 13.3 times, makes us even more comfortable. In addition to that, we’re happy to report that Resideo Technologies has boosted its EBIT by 38%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Resideo Technologies’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Resideo Technologies created free cash flow amounting to 18% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

Resideo Technologies’s interest cover was a real positive on this analysis, as was its EBIT growth rate. On the other hand, its conversion of EBIT to free cash flow makes us a little less comfortable about its debt. Looking at all this data makes us feel a little cautious about Resideo Technologies’s debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. The balance sheet is clearly the area to focus on when you are analysing debt.