The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, RingCentral, Inc. (NYSE:RNG) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

What Is RingCentral’s Debt?

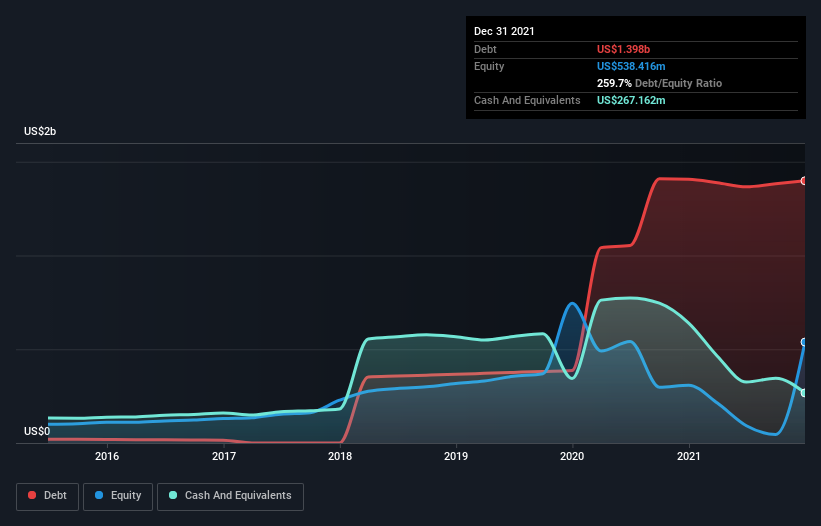

The chart below, which you can click on for greater detail, shows that RingCentral had US$1.40b in debt in December 2021; about the same as the year before. On the flip side, it has US$267.2m in cash leading to net debt of about US$1.13b.

A Look At RingCentral’s Liabilities

The latest balance sheet data shows that RingCentral had liabilities of US$526.3m due within a year, and liabilities of US$1.51b falling due after that. Offsetting these obligations, it had cash of US$267.2m as well as receivables valued at US$232.8m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$1.54b.

Given RingCentral has a humongous market capitalization of US$10.6b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if RingCentral can strengthen its balance sheet over time.

In the last year RingCentral wasn’t profitable at an EBIT level, but managed to grow its revenue by 35%, to US$1.6b. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

While we can certainly appreciate RingCentral’s revenue growth, its earnings before interest and tax (EBIT) loss is not ideal. To be specific the EBIT loss came in at US$302m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. However, it doesn’t help that it burned through US$233m of cash over the last year. So to be blunt we think it is risky. There’s no doubt that we learn most about debt from the balance sheet.