The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies International Money Express, Inc. (NASDAQ:IMXI) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

What Is International Money Express’s Net Debt?

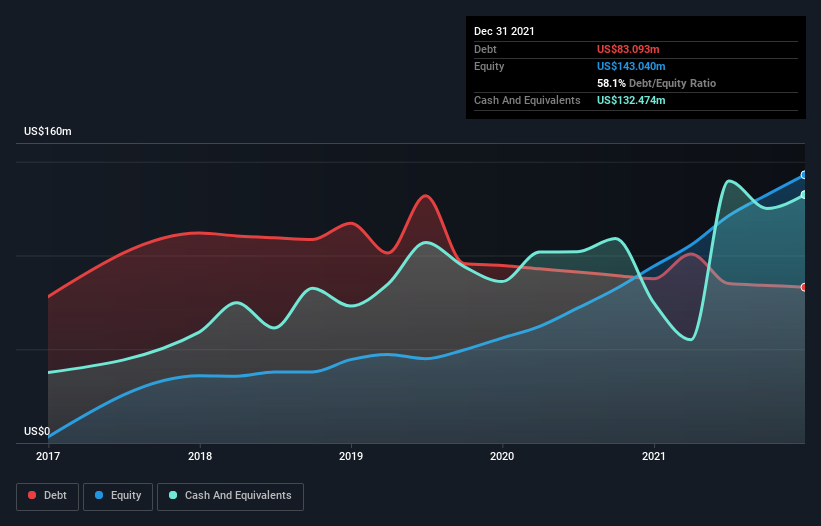

As you can see below, International Money Express had US$83.1m of debt at December 2021, down from US$87.6m a year prior. But on the other hand it also has US$132.5m in cash, leading to a US$49.4m net cash position.

A Look At International Money Express’ Liabilities

We can see from the most recent balance sheet that International Money Express had liabilities of US$116.9m falling due within a year, and liabilities of US$80.6m due beyond that. On the other hand, it had cash of US$132.5m and US$68.1m worth of receivables due within a year. So its total liabilities are just about perfectly matched by its shorter-term, liquid assets.

Having regard to International Money Express’ size, it seems that its liquid assets are well balanced with its total liabilities. So while it’s hard to imagine that the US$759.5m company is struggling for cash, we still think it’s worth monitoring its balance sheet. Simply put, the fact that International Money Express has more cash than debt is arguably a good indication that it can manage its debt safely.

On top of that, International Money Express grew its EBIT by 33% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if International Money Express can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While International Money Express has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the most recent three years, International Money Express recorded free cash flow worth 66% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

While it is always sensible to investigate a company’s debt, in this case International Money Express has US$49.4m in net cash and a decent-looking balance sheet. And it impressed us with its EBIT growth of 33% over the last year. So is International Money Express’s debt a risk? It doesn’t seem so to us. We’d be very excited to see if International Money Express insiders have been snapping up shares.