Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Mettler-Toledo International Inc. (NYSE:MTD) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Mettler-Toledo International’s Net Debt?

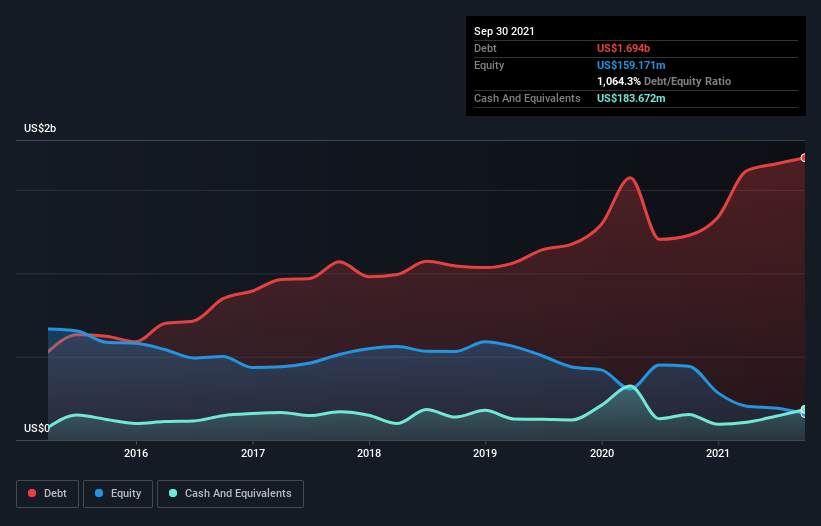

The image below, which you can click on for greater detail, shows that at September 2021 Mettler-Toledo International had debt of US$1.69b, up from US$1.23b in one year. However, it also had US$183.7m in cash, and so its net debt is US$1.51b.

How Healthy Is Mettler-Toledo International’s Balance Sheet?

The latest balance sheet data shows that Mettler-Toledo International had liabilities of US$1.00b due within a year, and liabilities of US$2.05b falling due after that. Offsetting these obligations, it had cash of US$183.7m as well as receivables valued at US$603.4m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$2.26b.

Given Mettler-Toledo International has a humongous market capitalization of US$35.5b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Mettler-Toledo International’s net debt is only 1.4 times its EBITDA. And its EBIT easily covers its interest expense, being 23.8 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Another good sign is that Mettler-Toledo International has been able to increase its EBIT by 29% in twelve months, making it easier to pay down debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Mettler-Toledo International’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Mettler-Toledo International produced sturdy free cash flow equating to 77% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Happily, Mettler-Toledo International’s impressive interest cover implies it has the upper hand on its debt. And that’s just the beginning of the good news since its EBIT growth rate is also very heartening. Overall, we don’t think Mettler-Toledo International is taking any bad risks, as its debt load seems modest. So the balance sheet looks pretty healthy, to us. When analysing debt levels, the balance sheet is the obvious place to start.