David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, US Ecology, Inc. (NASDAQ:ECOL) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does US Ecology Carry?

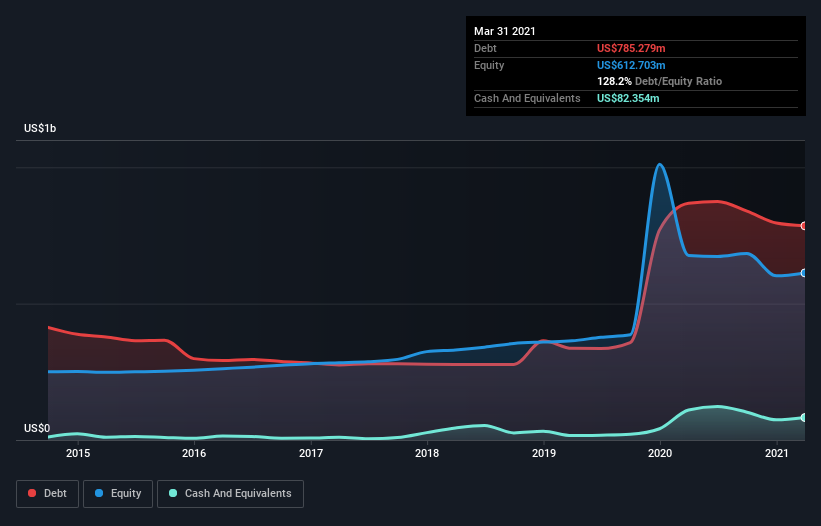

You can click the graphic below for the historical numbers, but it shows that US Ecology had US$785.3m of debt in March 2021, down from US$867.8m, one year before. However, it also had US$82.4m in cash, and so its net debt is US$702.9m.

A Look At US Ecology’s Liabilities

The latest balance sheet data shows that US Ecology had liabilities of US$165.4m due within a year, and liabilities of US$1.05b falling due after that. Offsetting these obligations, it had cash of US$82.4m as well as receivables valued at US$259.9m due within 12 months. So its liabilities total US$868.2m more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of US$1.13b, so it does suggest shareholders should keep an eye on US Ecology’s use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While US Ecology’s debt to EBITDA ratio (4.8) suggests that it uses some debt, its interest cover is very weak, at 1.3, suggesting high leverage. In large part that’s due to the company’s significant depreciation and amortisation charges, which arguably mean its EBITDA is a very generous measure of earnings, and its debt may be more of a burden than it first appears. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. Even worse, US Ecology saw its EBIT tank 51% over the last 12 months. If earnings keep going like that over the long term, it has a snowball’s chance in hell of paying off that debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine US Ecology’s ability to maintain a healthy balance sheet going forward. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, US Ecology recorded free cash flow worth 51% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

To be frank both US Ecology’s interest cover and its track record of (not) growing its EBIT make us rather uncomfortable with its debt levels. But at least its conversion of EBIT to free cash flow is not so bad. We’re quite clear that we consider US Ecology to be really rather risky, as a result of its balance sheet health. So we’re almost as wary of this stock as a hungry kitten is about falling into its owner’s fish pond: once bitten, twice shy, as they say. Even though US Ecology lost money on the bottom line, its positive EBIT suggests the business itself has potential.